The small-cap premium is one of the oldest return anomalies (or risk factors, if you’re so inclined) identified in the research literature. But after decades of analysis and mixed results, the idea that small company shares will outperform large caps also draws plenty of skepticism.

Earlier this year, for instance, Morningstar asked: Does the Small-Cap Premium Exist? Even if it does, it’s “unreliable,” advised an analyst in January. “Investors should not count on a small-cap tilt as a way to boost long-term performance.” Raising doubts about this corner of the market isn’t new—a 1999 study in The Journal of Finance, as one example, finds that the size effect evaporates after correcting for a “delisting bias.”

Have we been hoodwinked? Perhaps, although the degree of skepticism seems to be a cyclical affair. Casting aspersions on the strategy resonates whenever smaller stocks stumble in relative and/or absolute terms, which describes recent history. How does the small-cap premium compare over the longer term? Minds will differ, for the simple reason that we can torture the data to force any confession we choose. Tell me the outcome you’re looking for and I’ll provide the appropriate historical window.

That said, the standard performance summaries through yesterday (Dec. 10) don’t look encouraging, based on numbers published by Russell Investments. Across several trailing periods, the Russell 2000 Index (a popular US small-cap benchmark) trailed and/or matched large caps (Russell 1000).

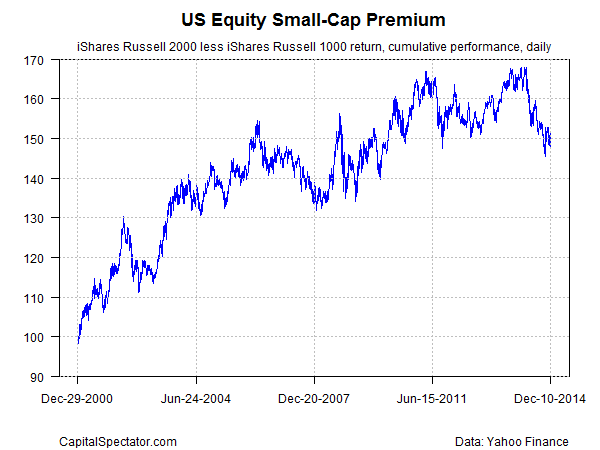

But before we close the door on this risk factor, consider how a real-world example via ETFs compares. As a simple test, let’s measure the spread for the daily return for the iShares Russell 2000 (IWM) less the iShares Russell 1000 (IWB) and use that as a basis for a buy-and-hold strategy with a start date as of Dec. 29, 2000. If there’s a cumulative advantage to small caps, this spread strategy will rise through time; if large caps prevail, the strategy will lose money. As you can see in the chart below, rumors of the small-cap premium’s death appear to be premature. This spread strategy is up roughly 50% since the end of 2000, although it’s been fading in recent months.

Is this definitive proof that the small-cap edge will endure in the years ahead? No, of course not, although it’s a strong piece of empirical evidence for rejecting the argument that the small-cap factor is dead and buried. By that standard, the recent weakness in small-caps looks like a rebalancing opportunity rather than the opening lines to a funeral march.

Try running the data on 20 years. You may not be convinced.

http://stockcharts.com/h-sc/ui?s=$RUT:$SPX&p=D&yr=20&mn=8&dy=0&id=p90219065209

hey james.

so the second chart shows a long/short strategy that is rebalanced daily? im just trying to better understand why the long/short strategy in the 2nd chart, say at the 10 year horizon doesnt show a -.3% (7.7-8%). is it just because one is annualized returns and one is cumulative returns? thanks!

d,

The second chart — the graph — isn’t a long/short strategy. Rather, it measures the cumulative performance spread on a daily basis. As an example, the chart has a starting date of Dec. 31, 2007, set to 100. The next trading day (1/2/2008) shows the returns for each fund as follows:

small cap: -0.009738372

large cap: -0.0111763863

The spread (-0.009738372 less -0.0111763863) is a net 0.001438014, and so the initial 100.0 index value rises to 100.14380 ((100*0.001438014)+100)