An ETF-Based Measure of Stock Price Fragility

Renato Lazo-Paz (University of Ottawa)

July 2023

A growing literature employs equity mutual fund flows to measure a stock’s exposure to non-fundamental demand risk – stock price fragility. However, this approach may be biased by confounding fundamental information, potentially leading to underestimating risk exposure. We propose an alternative estimation procedure incorporating readily available primary market data from exchange-traded funds (ETFs). Our proposed procedure significantly enhances the predictive power of fragility in forecasting stock return volatility. Moreover, we find that our measure captures the influence of increased ETF activeness while partially capturing the effect of institutional investors’ demand on price return volatility. Additionally, our analysis reveals a decrease in the explanatory power of mutual fund-based fragility. These results highlight the advantages of employing an ETF-based fragility measure that takes into account recent developments in the asset management industry, particularly the rise of passive investing.

Daily Archives: October 13, 2023

Macro Briefing: 13 October 2023

* Scalise withdraws from Speaker race, leaving House in limbo

* Would wider war in Middle East tip world economy into recession?

* Oil prices jump after US tightens sanctions on sales of Russian crude

* US jobless claims remain steady, holding near multi-decade low

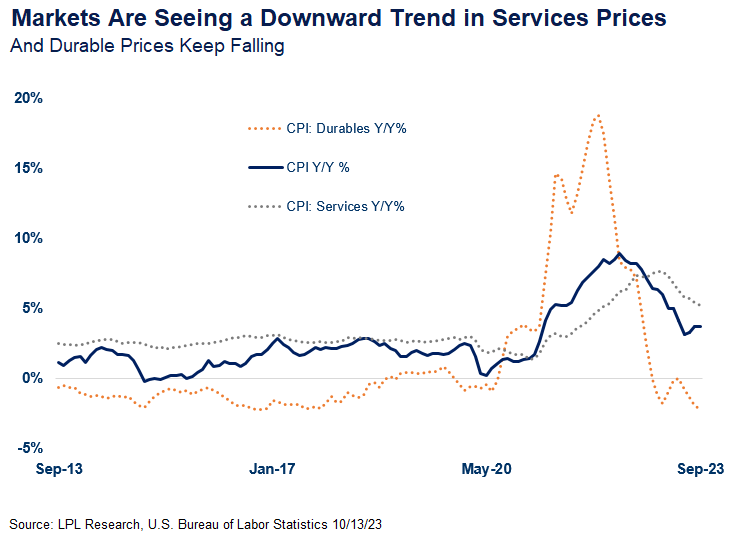

* US consumer price inflation unchanged at 3.7% annual pace in September: