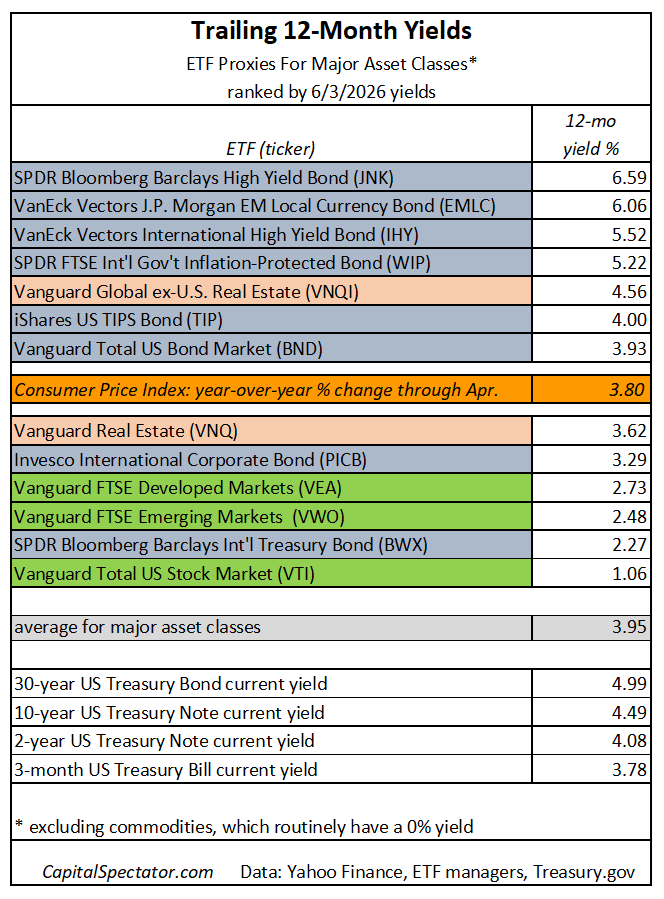

US junk bonds continue to post the highest trailing one‑year yields for the major asset classes, based on a set of ETFs through June 3. Roughly half of the funds are reporting payout rates above the current pace of annual consumer inflation.

The 6.59% trailing yield for the SPDR High Yield Bond ETF (JNK) remains the payout leader. On the opposite end of the spectrum, US stocks (VTI) are posting the lowest yield at 1.06%.

The highest‑yielding asset classes offer trailing yields above Treasuries, which top out at 4.99% for the 30‑year maturity.

For comparison, consumer inflation is running at 3.80% on an annual basis through April. Using that benchmark, about half of the major asset classes are generating positive real yields. The average trailing yield across all asset classes is 3.95%, slightly above the current inflation rate.

For readers eyeing these yields as a basis for asset allocation, the usual caveats apply. Trailing payout rates may or may not persist. Unlike the ability to lock in current yields on government bonds through a buy‑and‑hold strategy, historical payout rates for risk assets—such as those delivered via ETFs—can be misleading in real time because both payout amounts and share prices fluctuate. The table above is presented as a first step for comparing yields and considering how to structure a portfolio when the goal focuses on generating income.

One reason to be cautious when reviewing trailing yield is the ever‑present risk that whatever you earn in payouts from ETFs could be offset—or more than offset—by declining share prices. That’s why it’s essential to consider total‑return expectations when evaluating yield opportunities. For perspective on forward‑looking performance, you can start with the monthly updates of CapitalSpectator.com’s long‑term outlook for major asset classes.

The opportunity to earn yields above the “risk‑free” payout rates on US Treasuries may look appealing, but relatively high yields generally signal higher risks. That doesn’t mean it’s misguided to build a portfolio designed to maximize yield, but it’s rarely, if ever, a free lunch.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Trailing yields are always an interesting topic. Do you think they’ll stay low for a while?

Voxkasynopolska507, Your question is a reframing of: Where are markets headed? In the short run, it’s anyone’s guess, especially these days.

–JP

Interesting analysis (yields at the ETF level, rather than individual securities), which I don’t recall seeing before. I hope you will update it from time to time.