The new Fed Chair, Kevin Warsh, wants the bond market to take the lead in pricing interest rates—effectively shifting more of the central bank’s traditional role to market forces. The ongoing rise in real (inflation‑adjusted) yields suggests investors are doing exactly that in response to the recent jump in inflation.

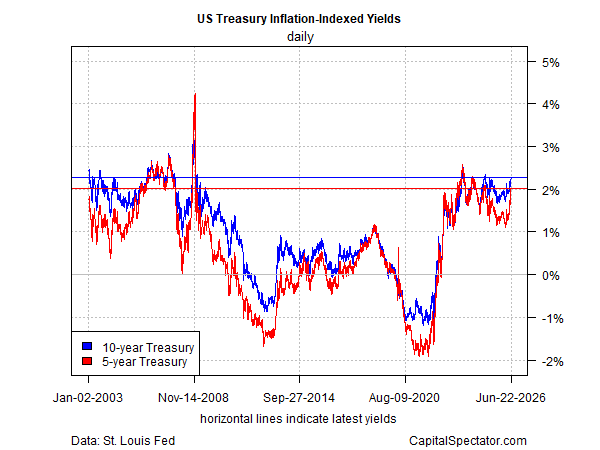

Consider real yields on Treasury Inflation‑Protected Securities (TIPS). At yesterday’s close, the 5‑year TIPS rate climbed to 2.01%, its first move above 2.0% in more than a year. That follows earlier breaks above the 2.0% threshold in longer maturities, including the 10‑year TIPS, now at 2.13%. At the far end of the curve, the 30-year TIPS yield is 2.75%.

By the standards Warsh laid out last week at his first press conference as Fed chair, higher real yields are part of the plan. In remarks widely interpreted as hawkish, he said that “inflation has been running well ahead of the Fed’s long‑stated inflation goal of 2%—that’s been going on for more than five years. Persistently high prices are a burden for the American people.”

The rise in real yields above 2% suggests the market is recalibrating and signaling that tighter policy may be needed. Warsh appears comfortable with that shift. As he put it last week: “I think financial markets perform best when they react to incoming data.”

Given the hotter inflation readings, higher real yields are the natural response. “The more that markets are paying attention to what’s happening in the real economy—deciding what’s good data and what’s less good data—the more financial markets can price what they believe is the most likely and what the tail risks are,” Warsh explained.

For investors, the chance to lock in real yields above 2% makes TIPS more appealing. As recently as Feb. 27, the 5‑year real yield was just 1.11%. But the war with Iran, which pushed up energy prices and inflation, has driven real yields sharply higher.

How long these elevated real yields persist, or rise further, is uncertain. While headline inflation is running much hotter because of the war, core inflation has been more subdued, giving the Fed room to consider whether rate hikes are actually necessary.

Fed funds futures are beginning to price in higher odds of hikes at upcoming meetings. But with Vice President Vance reporting “great progress” in talks with Iran, the conflict’s endgame coming into view, and energy prices falling, it’s unclear how much further real yields can rise without a new catalyst to worry the bond ghouls.