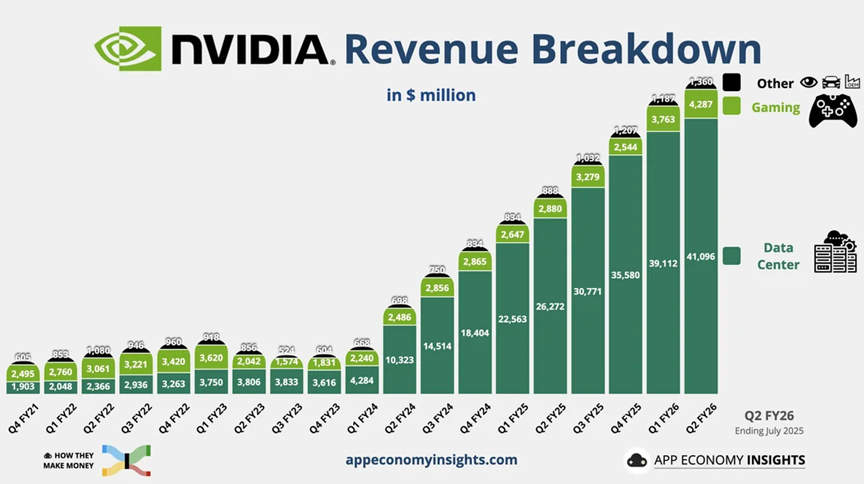

Chipmaker Nvidia reported better-than-expected earnings and revenue on Wednesday, a sign that AI-related investing remains strong. “The company is still growing over 50% [year on year] on their guidance at a $50B quarterly revenue run rate – that’s remarkable, even for the current valuation,” said David Wagner, head of equity at Aptus Capital Advisors. Matt Orton, head of advisory solutions at Raymond James Investment Management, said: “If anything, this just highlights that there’s a lot of durability to this (AI) trade… The businesses of these hyperscalers can continue to accelerate, and you’re not seeing any sort of sign of a slowdown being reflected in the results of Nvidia.”

Continue reading →