The Federal Reserve’s wait-and-see approach for monetary policy is starting to crack, or so markets are indicating. The central bank is still expected to leave interest rates unchanged at the next FOMC meeting in July, but confidence for a no-change decision has slipped recently while the estimated probability for a cut in September has increased.

Fed funds futures this morning are pricing in a 79% probability for standing pat next month, down from a near-100% estimate in recent weeks. Meanwhile, a September cut is estimated at a 90% probability at the moment.

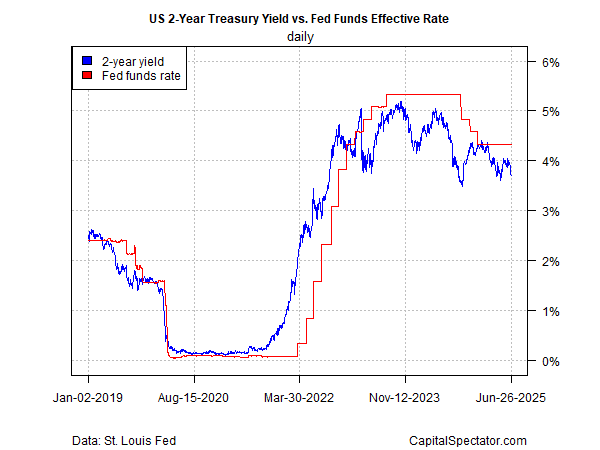

In a sign of how market expectations have turned increasingly dovish in recent days, the policy-sensitive US 2-year Treasury yield fell for a seventh-straight trading session on Thursday (June 26), settling at 3.70%, the lowest in nearly two months, according to Treasury.gov. The gap for the 2-year yield vs. the higher median Fed funds rate, in other words, continued to widen, which suggests that sentiment in the Treasury market is leaning into higher odds for an expected rate cut.

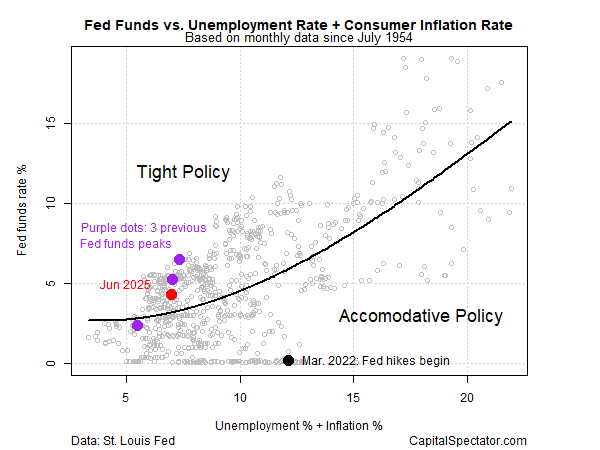

A simple model that compares inflation and unemployment against the median effective Fed funds target rate is still reflecting an moderately tight policy stance. The case for a cut in rates, in other words, appears to be warranted.

Meanwhile, Federal Reserve Chairman Powell this week reaffirmed that the central bank was still on track to keep rates steady. Citing uncertainty about the risk of inflation from tariffs, he reasoned: “Policy changes continue to evolve, and their effects on the economy remain uncertain,” via prepared remarks given as testimony to Congress. “For the time being, we are well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.”

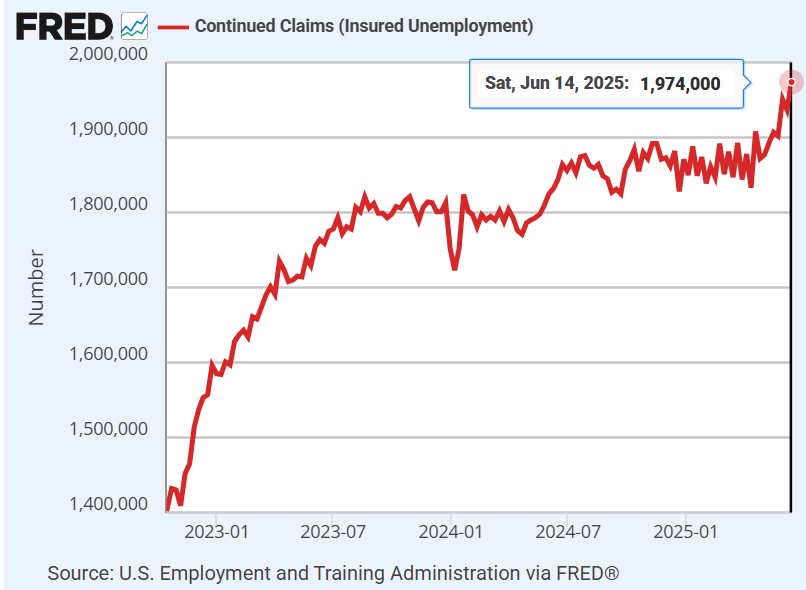

Another factor that’s influencing market sentiment: the labor market may be showing signs of weakening, based on initial and continuing jobless claims. Although initial claims pulled back for a second week, after rising to the highest level since October, continuing claims are still rising and jumped to the highest level in 3-1/2 years.

“The data are consistent with softening of labor market conditions, particularly on the hiring side of the labor market equation,” said Nancy Vanden Houten, lead economist at Oxford Economics. “For now, we don’t think the labor market is weak enough to prompt the Fed to cut rates before December, but the risk is increasing that once the Fed starts to lower rates, it will have some catching up to do.”

Meanwhile, President Trump continues to pressure the Fed to cut rates. A report this week said he is considering naming Powell’s successor sooner than expected in an effort to influence monetary policy. Powell still has 11 months to go before his term is up, but markets may soon have to start factoring in comments from a shadow Fed chair if Trump nominates someone early.

“This is a terrible idea, sure to annoy and confuse financial markets if there are two Fed Chairs,” said Greg Valliere, chief US policy strategist at AGF Investments. Kathryn Judge, a professor at Columbia Law School who researches financial markets and central banking, advised: “It all depends on just how loyal this person is expected to be to Trump. But we don’t we know what the ramifications would be or what they’d be willing to do, because this is unprecedented.”

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report