Nearly every corner of the major asset classes took a beating in February, courtesy of coronavirus-related worries. Only investment-grade US bonds, US inflation-indexed government bonds and cash bucked the risk-off sentiment. Otherwise, red ink swept across markets near and far.

Continue reading

Macro Briefing | 2 March 2020

OECD: Covid-19 is biggest threat to global economy since financial crisis: OECD

A degree of calm returns to Asian markets on Monday: Reuters

Syria’s war escalates as Turkey responds to attack with drone strikes: BBC

Greece ends asylum as migrants mass on its border with Turkey: NY Times

North Korea fires two missiles into Sea of Japan: CNN

US and Taliban sign deal to end 18-year war in Afghanistan: BBC

Caixin China General Manufacturing PMI crashed in February: IHS Markit

Eurozone mfg recession eased in Feb but Covid-19 weighs on outlook: IHS Markit

US consumer spending slowed in January: Reuters

US Consumer Sentiment Index rose in February, near post-recession high: UoM

Chicago PMI edged up in Feb but still below neutral 50 mark: Chicago PMI

Comparing last week’s stock market loss with previous 5-day declines: CNBC

Book Bits | 29 February 2020

● The Long Deep Grudge: A Story of Big Capital, Radical Labor, and Class War in the American Heartland

By Toni Gilpin

Summary via publisher (Haymarket Books)

This rich history details the bitter, deep-rooted conflict between industrial behemoth International Harvester and the uniquely radical Farm Equipment Workers union. The Long Deep Grudge makes clear that class warfare has been, and remains, integral to the American experience, providing up-close-and-personal and long-view perspectives from both sides of the battle lines. International Harvester – and the McCormick family that largely controlled it – garnered a reputation for bare-knuckled union-busting in the 1880s, but in the 20th century also pioneered sophisticated union-avoidance techniques that have since become standard corporate practice. On the other side the militant Farm Equipment Workers union, connected to the Communist Party, mounted a vociferous challenge to the cooperative ethos that came to define the American labor movement after World War II.

Continue reading

Welcome To Financial And Economic Re-education Camp

For the casual observer, the stock market’s rapid slide looks like madness. It was, after all, only last week that the S&P 500 closed at a record high. Six trading days later, the market has lost 12% (as of Feb. 27)–the fastest correction on record for declines of 10%-plus. But before we let recency bias take complete control of our minds, let’s consider if there’s a method in Mr. Market’s madness.

Macro Briefing | 28 February 2020

World Health Organization: coronavirus outbreak at “decisive point”: BBC

World markets set for worst week since financial crisis: CNBC

Profiling stock market corrections since World War II: CNBC

Dozens of Turkish soliders killed in Syria by missile strike: NY Times

Turkey will no longer stop Syrian refugees from migrating to Europe: Reuters

Philly Fed’s ADS business cycle index still reflects modest growth: PF

Revised Q4 GDP data for US remains unchanged at +2.1%: Reuters

US durable goods orders edged lower in January: MW

US jobless claims rose last week but remain near historic lows: CNBC

World economy headed for worst year since financial crisis: BBG

Forecasting Global Reported Cases Of Coronavirus

Healthcare risk isn’t usually the leading factor in economic analysis, but the rise of coronavirus (Covid-19) has changed the focus and the calculus. Covid-19, in short, is on everyone’s short list for modeling the near-term macro outlook, in the US and around the world. At some point this, too, shall pass and something approximating a “normal” environment for economic analysis will return. Meantime, the uncertainty surrounding Covid-19 is shredding the usual macro modeling efforts. With that in mind, here begins a preliminary and evolving effort by CapitalSpectator.com for projecting the near-term path of cumulative reported cases of Covid-19 on a global basis, using a proprietary econometric forecasting methodology.

Macro Briefing | 27 February 2020

Govt’s around the world take more aggressive stance on coronavirus: Reuters

Trump announces VP Mike Pence to lead US coronavirus response: USA Today

First US coronavirus infection reported not linked to int’l travel: NY Times

New coronavirus cases reported in S. Korea tops China for first time: SCMP

US-S. Korea military drills on hold due to coronavirus: Reuters

Is the stock market selloff just getting started? Bloomberg

Eurozone economic sentiment rebounds in Feb–fourth month of improvement: EC

New US home sales surged to 13-year high in January: Bloomberg

US Economy Still Expected To Expand At Moderate Pace In Q1

The coronavirus is weighing on economic estimates around the world and it’s likely that the US will eventually feel some of this pain. The degree of the macro price tag for America remains a guessing game at this point. As a baseline, we can monitor how the first-quarter nowcasts evolve in the days and weeks ahead. On that front, the latest numbers point to a slightly softer increase in output for Q1 vs. the previous quarter.

Macro Briefing | 26 February 2020

Global equities continue to slide on Wed amid escalating coronavirus worries: WSJ

US prepares for spread of coronavirus: Reuters

Several European countries announce coronavirus cases: BBC

Fed’s Clarida: “still too soon” to discuss a rate cut: MW

Globalization faces a new front of attack with coronavirus: NY Times

JP Morgan warns investors on climate-change risk: Bloomberg

US home price growth picked up in Dec, marking eighth year of price gains: Mstar

Mfg activity ticked lower in February in Richmond Fed district: Richmond Fed

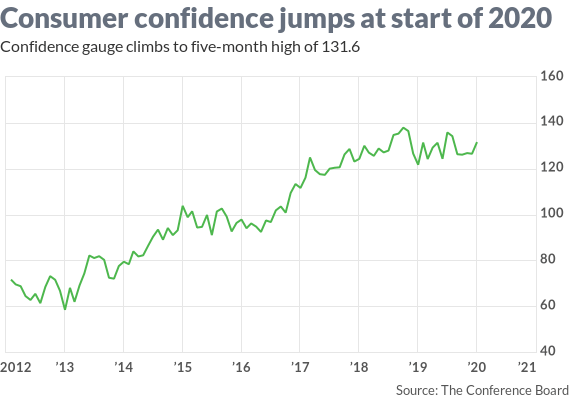

US Consumer Confidence Index rose in January to five-month high: MW

Assessing The Damage After Monday’s Sharp Decline In Stocks

Well, that was painful. The increasingly hazy risk outlook linked to the coronavirus outbreak inspired a 3.35% haircut in the US stock market (S&P 500). The tumble was certainly a bracing counterpoint to the idea that sunny optimism is the only game in town. But before we let recency bias flip to the opposite extreme, let’s review where we stand after yesterday’s smackdown.