In a new article from Institutional Investor—“Market Timing Is Back In The Hunt For Investors”–AQR Capital Management reviews the case for market timing and finds an encouraging track record. Citing the historical record from 1900, AQR’s Cliff Asness and two colleagues outline what is effectively a century-plus backtest of the value and momentum factors. In line with analysis from other researchers, they find that the numbers favor a degree of dynamic portfolio management for adjusting asset allocation through time based on this dual-factor framework. There’s nothing particularly new here, at least for anyone who’s familiar with the research on the topic of tactical asset allocation (TAA) and the related subjects. Nonetheless, this is a worthwhile read if only because it provides a long-run perspective on how the application of value and momentum factors provide a powerful foundation for managing an asset mix through time.

The authors are careful to point out that no one should confuse the results with a clear-cut case that market timing is easy. The standard caveats apply, they emphasize. Although the rearview mirror appears to provide an obvious roadmap for dynamic asset allocation, hindsight bias is probably making the process appear easier than it’s likely to be in real time going forward. For instance, it’s one thing to look back over a 100-plus-year period and proclaim that the turning points for valuation extremes are conspicuous. But investors in earlier generations didn’t have the benefit of knowing what we know now and so the ability to exploit the value and momentum factors in years past may have been limited and perhaps even missing altogether as a practical matter.

That’s a clue for wondering if we’re still in the dark to a degree because the future’s always uncertain. This may be an especially problematic issue for the value factor if assets are being repriced at a higher level generally compared with decades past. In other words, assets that appear cheap or expensive based on previous standards may no longer apply.

But those are standard warnings that apply to all backtests. Past performance is no guarantee of future results. Blah, blah, blah and caveat emptor… as usual. No less applies to a buy-and-hold strategy, by the way, and so everyone’s in the same boat. That said, the article makes a powerful case for combining the value and momentum factors in an asset allocation framework. Applying any one of the three is isolation of the other two runs up against serious obstacles; deploying all three as part of a larger strategic whole, on the other hand, forms the basis of a formidable toolkit for managing risk and generating attractive returns.

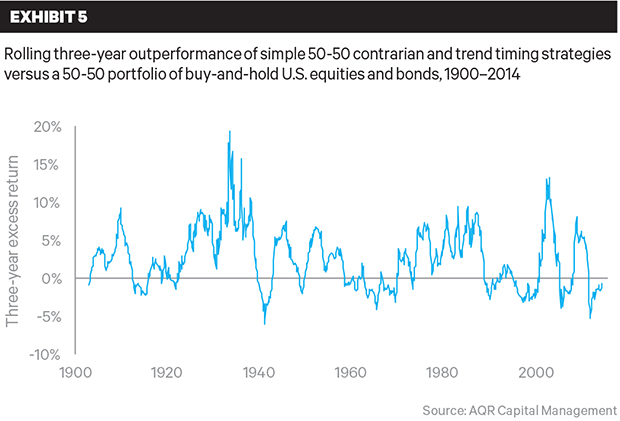

As an example, Asness and company point to the rolling 3-year performance for a 50/50 asset mix of US stocks and bonds since 1900 using a value and momentum strategy. Summarizing the results (shown in the chart below), the authors observe that “there are plenty of 3-year periods in which the full combo approach subtracts value (and we know good things get abandoned way too often when they suffer for three to five years). But at this horizon it adds considerably more often than it doesn’t, and historically it has been reasonably well behaved—that is, no superfat tails in either direction.”

We’ve heard various forms of this advice before, of course, and from a range of sources, including AQR’s research. For instance, the 2013 paper that Asness co-authored on the matter of combining the value and momentum factors across asset classes—“Value and Momentum Everywhere”—is a staple for interpreting a modern view of multi-factor investing. Meanwhile, Andreas Clenow makes a persuasive case in his recent book Following the Trend for deploying a momentum strategy across asset classes to minimize the inevitable failure that harasses individual trades. And, of course, there’s a deep pool of research that’s been inspired from Meb Faber’s influential analysis on using moving averages to generate signals for tactical asset allocation–“A Quantitative Approach to Tactical Asset Allocation”.

.

The new article builds on the existing literature, offering deeper perspective and offering some advice on how to extend the research for perhaps superior results in real-world money management: “Other factors (for example, carry in the form of a steep yield curve for bonds, relative valuation between stocks and bonds, some macro indicators) and other forecasting methodologies may be attempted, though you risk overfitting in exchange for attempted improvement.”

For all the potential for enhancing a static asset allocation program with a dynamic approach there are some obvious things that you shouldn’t do, the authors warn. That includes going to extremes with the asset adjustments. Moving from aggressive risk-on postures to all-cash positions and vice versa in a short period is impractical and probably ill-fated. There’s a supportive research pool for TAA, but only in a modified degree. Nothing’s perfect in the realm of investing and so even the most-compelling backtested factors will suffer failure at times. This is especially true for the value factor, which can remain out of favor for years. The solution is to embrace moderation by combining factors, investing across asset classes, and never betting the house on any one signal/asset class at any one point in time.

The good news is that there’s fertile ground for developing a customized dynamic asset allocation plan that matches a particular set of investment goals, risk tolerance, etc. The logic arises directly from analyzing market history. As Asness and his co-authors remind, “when prices look cheap versus a reasonable metric, buy a bit more. When they have been trending up, buy a bit more. Of course, also do the opposite, and average both these approaches, doing the most when they agree. Do it in both stocks and bonds.”

Is that the last word on designing a robust portfolio strategy? No, but it’s a solid beginning, which is an essential ingredient for engineering successful outcomes. There are still no sure bets, but the value+momentum+asset allocation proposition has become the new standard for evaluating a prudent approach to investing. Can you do better? Perhaps, but you face a high bar for developing an alternative and convincing line of analysis by way of empirical research.

Pingback: Quantocracy's Daily Wrap for 11/12/2015 | Quantocracy

Pingback: News Worth Reading: November 13, 2015 | Eqira