Yesterday’s verdict by the Federal Reserve to leave its policy rate unchanged at the zero-to-0.25% target–a policy that’s been in place for six years–has inspired speculation that the European Central Bank (ECB) will be forced to up its game with monetary stimulus. The crowd certainly appears to be making bets in that direction–Bloomberg reports that European bond prices surged today in reaction to yesterday’s announcement in Washington. Why? Laurence Mutkin, global head of Group-of-10 rates strategy at BNP Paribas, advises that the Fed’s dovish decision has ramifications for the ECB. “We think during the fourth quarter [the ECB’s] going to announce an extension of QE,” he explains.

ING Bank economist Carsten Brzeski agrees, telling The Wall Street Journal that “the ECB will now be confronted with a further strengthening of the euro and probably pushed closer to stepping up QE. To some extent, the Fed’s inaction could force new ECB action.”

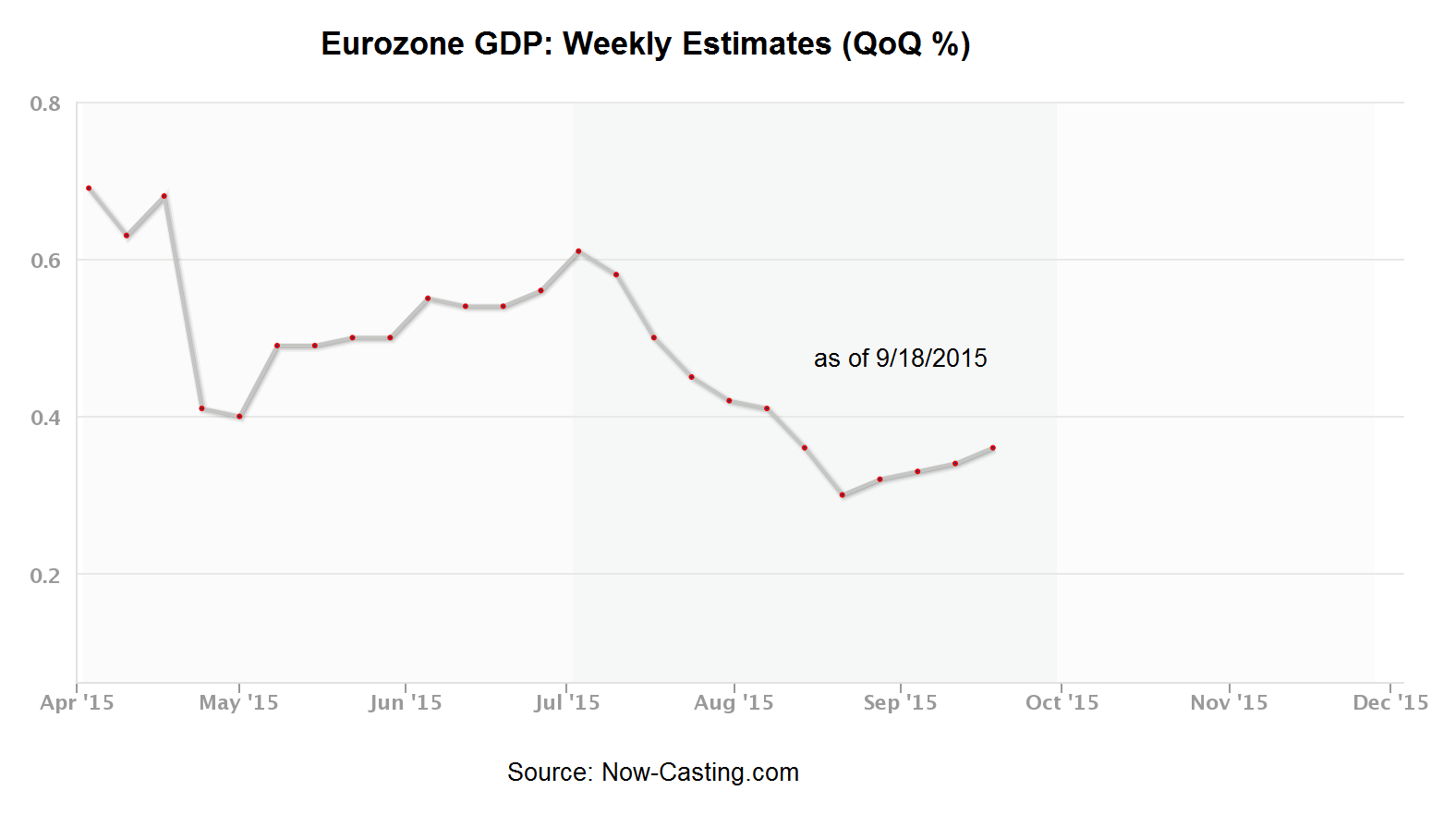

Perhaps, but such a decision will in part rely on how Europe’s modest economic recovery fares in the weeks ahead. For now, there’s still a positive wind blowing, based on today’s weekly estimate of third-quarter GDP growth for the Eurozone. It’s a modest and precarious growth bias, but it’s still moving in a productive direction.

Today’s weekly update for Eurozone Q3 GDP growth ticked up to 0.36%, according to Now-casting.com. The fractionally higher estimate marks the fourth straight improvement. The obvious caveat: the progress is minimal and the current estimate is slightly below Q2’s 0.4% GDP rise over the previous quarter, according to Eurostat’s official data. But weak progress is still better than backsliding.

The question, of course, is whether the sluggish improvement in Europe’s growth expectations will continue? To be determined, as they say. The near-term outlook can be described as cautiously optimistic, at least by the standards of what passes for growth in the Eurozone these days.

Unfortunately, there’s not a lot of confidence at the moment that upbeat signals in the here and now will survive. The Bank of England’s chief economist Andy Haldane summarized the challenged framework that’s weighing on the outlook in the wake of the Fed’s decision to keep its policy target at zero:

If global real interest rates are persistently lower, central banks may then need to think imaginatively about how to deal on a more durable basis with the technological constraint imposed by the zero lower bound on interest rates. That may require a rethink, a fairly fundamental one, of a number of current central bank practices.

Radical strategies, in other words, may again be in vogue when it comes to plotting the course ahead in monetary temples across the globe. But at this late date what can a central banker do for an encore when so many of the tricks have already been played–with mixed results? The rush back into government bonds today (on both sides of the Atlantic) suggests that the crowd’s not convinced that there’s an encouraging answer waiting in the wings.