Several months ago I reviewed the case for thinking that the long-suffering value factor for US equity investing was in the process of reviving. At the time, the evidence was sketchy but the outlook was encouraging. Fast forward to early August and the bullish trend looks a bit stronger for this corner of equities.

All the usual caveats apply, of course, but the fact that the upward bias for the value factor is intact is a positive if preliminary sign. Consider, for example, how a pair of ETFs representing a large-cap value portfolio (iShares Russell 1000 Value (IWD)) and its growth counterpart (iShares Russell 1000 Growth ETF (IWF)) have fared this year. Although growth retains a wide lead over value year to date, it’s notable that value’s recent underwater performance in 2018 has given way to a modest gain through yesterday’s close (August 6).

It’s premature to read too much into value’s modest rally of late, but for the year IWD is up 2.5%. Perhaps more importantly, value’s nascent bull run in positive terrain in 2018, fragile though it may be, has been ongoing for nearly a month. Measured from the recent bottom in the spring, IWD’s revival looks even stronger.

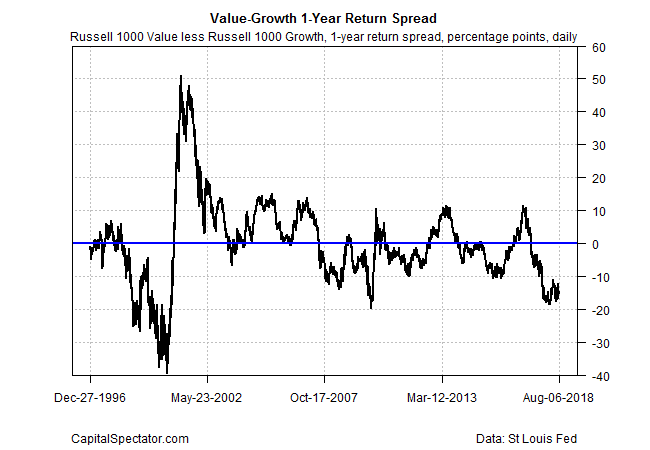

Nonetheless, value’s latest pop still leaves the risk factor’s performance deep in the red vs. growth, as defined by the rolling one-year return spread for the Russell 1000 Value Index less Russell 1000 Growth. Indeed, value is currently behind growth by roughly 15 percentage points for the trailing one-year window – close to its deepest relative setback since the last recession ended.

The key takeaway: there’s still a long road ahead for value’s revival, at least if you’re keeping score by way of growth’s relative performance.

By some accounts, however, the recovery may soon run out of road. “We see a stronger macro case for the yield curve to continue its flattening trend which is likely to be a headwind for further value out performance if this relationship holds,” warns Mayank Seksaria, chief macro strategist at Macro Risk Advisors, in a note to clients.

Perhaps, although the latest economic profile for the US looks solid, as summarized by the strong acceleration of growth in the second quarter. Employment growth in July was softer than expected, but as I pointed out in last week’s update: the annual trend in private-sector job creation remained moderately strong and healthy last month.

The potential for macro blowback from the simmering trade war between the US and China is a risk factor. Ditto for the recent weakness in US housing data.

But the big-picture trend for the US economy remains upbeat – a profile that was reaffirmed in the August 5 edition of the US Business Cycle Risk Report.

It’s still early for making confident estimates for third-quarter GDP activity, but the preliminary guesses are encouraging, for whatever that’s worth. In particular, the Atlanta Fed’s August 3 GDPNow model projects a 4.4% increase in Q3 output – slightly higher than Q2’s strong 4.1% gain. The equivalent nowcast via the New York Fed is substantially softer at 2.6%, but the average of the two – a roughly 3.4% rise – is still a solid advance and more than enough to keep the US economy humming.

To the extent that value’s rebound requires the fuel of a positive macro trend, it’s too early to say the jig is up. But with the US expansion currently logging in as the second longest on record, (based on NBER data that begins the 1850s), some analysts say that the macro clock is ticking. Maybe, but if we’re using published economic data the outlook is still bright for value.

Regardless of your near-term view of the economy, there’s a good case for arguing that value investing should only be considered as a long-term strategy rather a tactical play.

“If you believe in the long-term value premium, you can make a case this is actually the time to be increasing value exposure,” says Alec Lucas, senior analyst at Morningstar Research Services. “You can see extended underperformance for another two years, but [you’ll] have a good chance of doing well over the next five to seven years.”

A New Book From The Capital Spectator:

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: Value Investing Reviving? - TradingGods.net

Pingback: Market Remains in a Narrow Trading Range - TradingGods.net