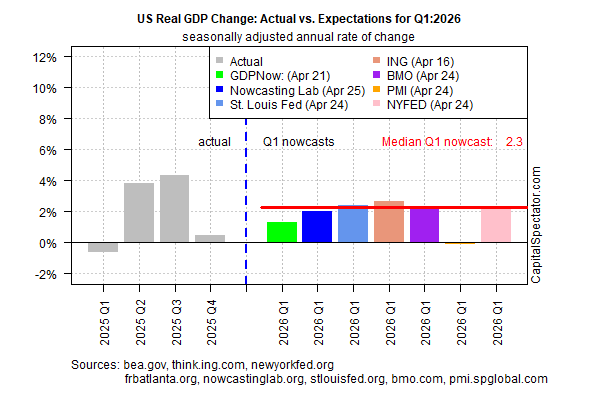

Economic activity appears set to recover in this week’s initial estimate of first‑quarter GDP, based on the median nowcast from several estimates compiled by CapitalSpectator.com. But any celebration will be muted as the stalemate in the war between the US and Iran lingers, casting a shadow over the inflation and growth outlook for Q2 and beyond.

Focusing on Thursday’s GDP release from the Bureau of Economic Analysis points to a pickup in output following Q4’s tepid 0.5% rise. This week’s Q1 data, by contrast, is projected to increase to an annuallized 2.3% rate via the median estimate.

The path ahead is fraught due to the slow‑moving but ongoing blowback from the Middle East turmoil, which has blocked energy exports from the Gulf. The conflict’s continuing reverberations are expected to lift inflation and slow economic growth. The US is better positioned than Europe and much of Asia, but America isn’t immune.

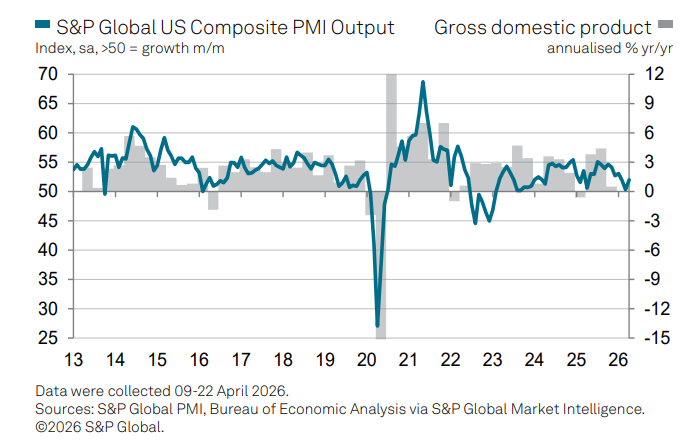

Survey data for April highlight US resilience, at least in relative terms. “US business activity growth recovered slightly in April, having slowed to near‑stagnation in March following the outbreak of war in the Middle East,” reports S&P Global via the US Composite PMI Output Index, a GDP proxy. “However, the overall pace of expansion remained subdued, most notably in the services economy, where demand faltered.”

The stalemate in the war suggests that a resolution could be brewing. But until energy exports from the Gulf resume, the headwinds for growth—and the tailwinds for inflation—will persist and strengthen.

“A diplomatic settlement to the Iran war at some point would bring some immediate relief,” forecasts the Washington Center for Equitable Growth, a think tank. “But extensive physical destruction to critical infrastructure in Iran and around the Persian Gulf means US economic growth will likely continue to suffer over the medium term to long term.”

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report