The Federal Reserve is expected to keep its target interest rate unchanged in today’s policy announcement, but the stable outlook belies the unsettled inflation picture that’s keeping the bond market on edge.

Visibility for the rate outlook at today’s Fed meeting, by contrast, is clear as a bell. Fed funds futures are pricing in a 100% probability that the target rate will remain at its current 3.50%–3.75% range. After that, the clarity fades.

The bond market is struggling to price in the twin threats of higher inflation and slower economic growth—the dual effects of the Middle East turmoil that has elevated energy costs. The odds of a quick resolution remain low, a calculus reaffirmed after President Trump on Tuesday told aides “to prepare for an extended blockade of Iran, U.S. officials said,” according to The Wall Street Journal.

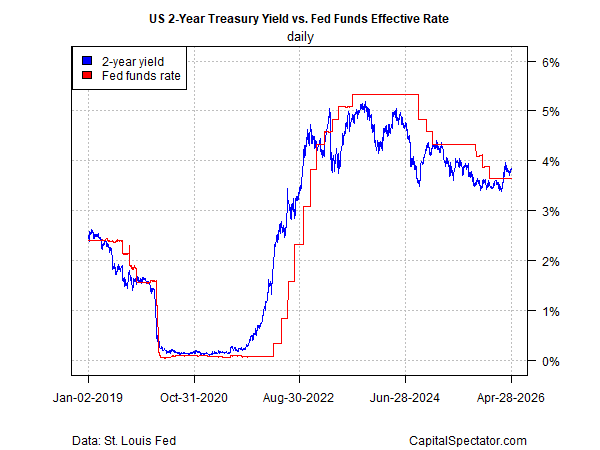

U.S. Treasury yields have increased recently but have pulled back from the peak that followed the start of the war on Feb. 28. The market is still flirting with the possibility of rate hikes, based on the policy‑sensitive 2‑year yield, which continues to trade above the effective Fed funds rate. That’s an indication that investor sentiment is pricing in modest odds that the central bank will be forced to raise interest rates at some point in the near term.

But not yet—and perhaps not for the next several FOMC meetings, or so Fed funds futures suggest.

The inflation bump has already begun and will likely persist in the near term. The Consumer Price Index (CPI) surged in March to a 3.3% year‑over‑year pace, up sharply from February’s 2.4%, driven by spiking energy costs. It’s unclear whether inflation will continue rising, but a safer bet is that it holds steady above 3% for now.

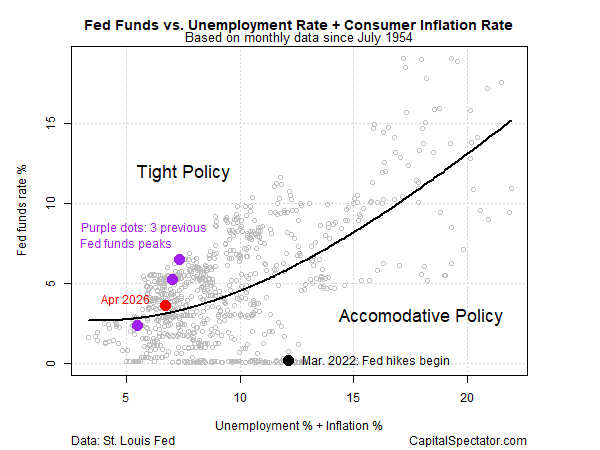

The Fed still still has some leftover ammunition in its policy toolkit in the form of a mildly hawkish bias, based on a simple model that compares the target rate to unemployment and inflation—the two components of the central bank’s dual mandate. On that basis, policy is slightly tight. The question is whether that will suffice in the months ahead, as the inflationary effects of the war—and now stalemate—in the US–Iran conflict endure.

A complicating factor is that the blowback from Middle East turmoil will weigh on global economic activity, which will spill over into the U.S. to some degree. If output slows enough, that could offset the need to hike rates.

Exactly how the twin shocks of higher inflation and slower growth will play out remains uncertain, thanks to the fog of war (stalemate), which is why the bond market—and the Fed—are playing a wait‑and‑see game.

“On the dual mandate, they’d say we’re roughly at a stable labor market,” Roger Ferguson, an economist and former Fed vice chair, told CNBC. “On the inflation side of the mandate, [there’s] a lot more work to be done with a sticky 3% [inflation rate], and I hope they argue, ‘we’re going to sit tight for a little while to see how this all plays out.’”

Two real‑time proxies on my short list for monitoring these risks are the 10‑year Treasury yield and the price of crude oil. The 10‑year yield closed yesterday at 4.35%, still comfortably below the intraday peak of nearly 4.50% since the war’s start, but the benchmark rate is drifting higher again. As it moves closer to the previous peak—and certainly if it breaks above it—that will signal that the market is demanding a higher inflation premium, which in turn will put more pressure on the Fed to hike.

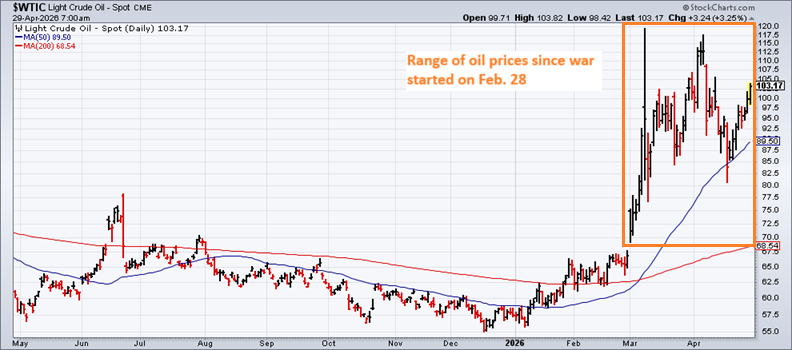

A similar calculus applies to crude oil, based on the US benchmark (West Texas Intermediate). The price closed yesterday above $103 a barrel. That’s still below the $120 peak set in the early days of the war, but prices are trending up again. If the market begins to test the upper range set during the war, that should be viewed as a sign that inflation pressures will persist, if not intensify, for longer than expected.

In the end, the Fed may be standing still, but the markets certainly aren’t. With inflation simmering and geopolitical tensions refusing to fade, investors are left navigating a landscape where every data point feels like a potential turning point. The calm of today’s decision may not last long.