The bond market is losing faith that inflation risk from the Middle East conflict will be contained and fade quickly. The Federal Reserve’s monetary policy is still in wait‑and‑see mode, but several key Treasury yields aren’t waiting to see what happens.

Jerome Powell, in his appearance yesterday as Fed chair, presided over the central bank’s widely expected announcement that it would leave its target rate unchanged at a 3.50%–3.75% range. The Fed, in its policy statement, noted that “inflation is elevated, in part reflecting the recent increase in global energy prices.”

Powell, responding to a question about war‑driven price surges at Wednesday’s press conference, said “it hasn’t even peaked yet.” He added: “I think we’d want to see the backside of that and progress on tariffs before we even thought about reducing rates. If we need to hike, we will; we will certainly signal that,” but not now.

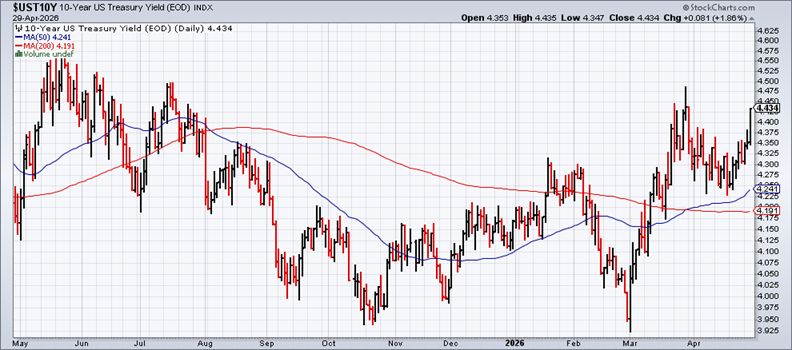

The Treasury market is starting to move on from waiting. The 2‑year yield, which is widely monitored as a market‑based outlook on policy, shot up to just under 3.97%, close to the wartime peak set early in the conflict.

The benchmark 10‑year yield also rose, jumping to 4.34%, which is likewise close to its wartime peak.

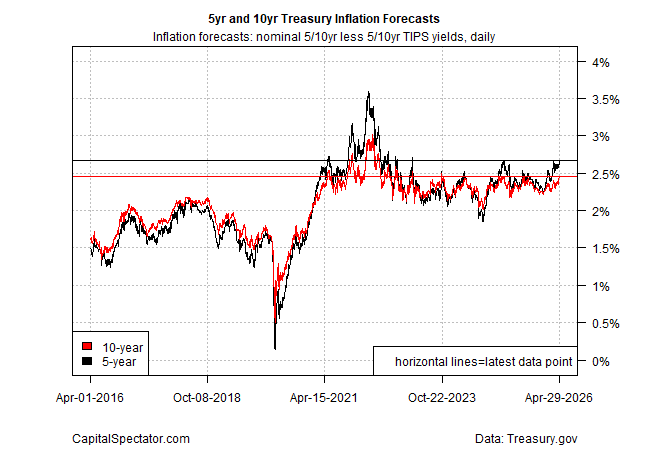

The Treasury market’s implied inflation forecasts are also rising again, based on the spread between nominal rates and their inflation‑indexed counterparts. Notably, the forecast via the 5‑year maturity increased to 2.67% yesterday, setting a new peak since the war began and widening the gap further relative to the Fed’s 2% inflation target.

Despite the mounting inflation worries in the Treasury market, the Fed is expected to keep rates steady through the end of the year, based on Fed funds futures.

Meanwhile, oil prices remain elevated. The U.S. benchmark (West Texas Intermediate) traded well above the $100‑a‑barrel mark for a second day and remains close to its wartime peak. Energy costs have already lifted consumer inflation in March due to surging energy prices, and a repeat performance is expected for the April data.

The growing mismatch between a Fed sitting on its hands and a worried bond market won’t last. The question is which side will blink first. Only one side gets to be right about inflation. The key variable, of course, is how the Iran conflict plays out, and for the moment a stalemate endures as the US and Iran hold fast to their respective views that they can wait each other out. Meantime, the inflation clock is ticking.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report