Payrolls for US companies increased by a seasonally adjusted 185,000 in July, which is moderately below Econoday.com’s consensus estimate for a 210,000 advance. The gain marks the smallest rise in three months, according to this morning’s release of the ADP Employment Report. Meanwhile, the year-over-year pace continued to weaken, sliding to a 2.26% gain for the year through last month—the slowest annual growth rate in more than a year.

“Job growth is strong, but it has moderated since the beginning of the year,” said Mark Zandi, chief economist of Moody’s Analytics, which produces the data in collaboration with ADP. “Layoffs in the energy industry and weaker job gains in manufacturing are behind the slowdown. Nonetheless, even at this slower pace of growth, the labor market is fast approaching full employment.”

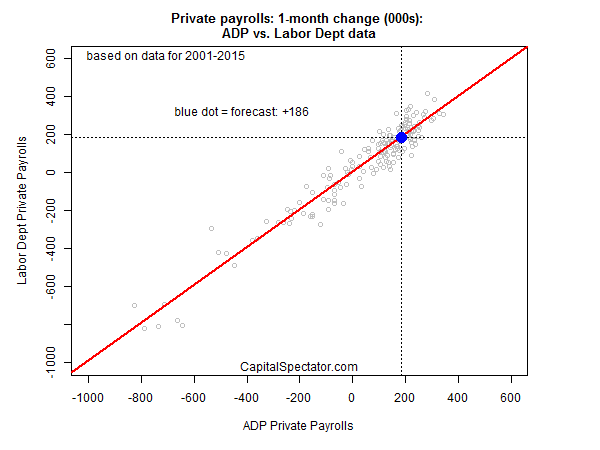

Nonetheless, today’s update raises questions about Friday’s official payrolls release from the Labor Department. Econoday.com’s consensus forecast sees the government’s estimate of private payrolls rising by 210,000 in July—modestly below June’s 223,000 advance.

Should Friday’s projection be revised down in the wake of today’s ADP data? Yes, according to a linear regression model that uses the historical relationship between the government and ADP data sets for predicting Washington’s estimate. Factoring in today’s ADP release to forecast Friday’s update (Aug. 7) points to a rise of 186,000 workers in the private sector for July—moderately below the current consensus estimate of 210,000.

The standard caveat is that the ADP numbers aren’t always a reliable measure for what to expect for government data in the short run. Nonetheless, today’s release implies that the odds for an upside surprise on Friday don’t look promising.