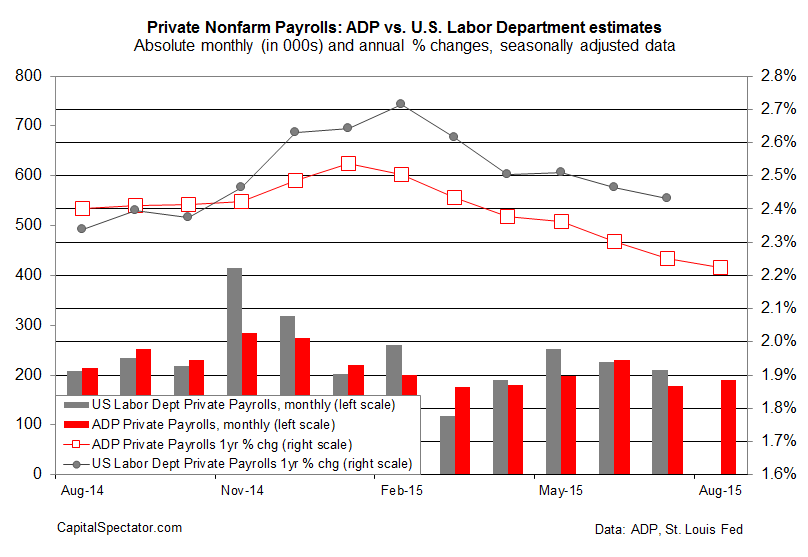

Payrolls at US companies increased by a moderate 190,000 (seasonally adjusted) in August, according to this morning’s monthly release of the ADP Employment Report. The respectable if not particularly impressive gain is slightly below Econoday.com’s consensus forecast for a 210,000 advance. Meanwhile, last month’s rise translates into another round of easing for the year-over-year rate. Nonetheless, today’s numbers are strong enough to fend off worries that a recession is imminent for the US.

“Recent global financial market turmoil has not slowed the US job market, at least not yet,” said Mark Zandi, chief economist of Moody’s Analytics, which publishes the data in connection with ADP. “Job growth remains strong and broad-based, except in the energy industry, which continues to shed jobs. Large companies also remain more cautious in their hiring than smaller ones.”

Yet it’s also clear that the pace of job creation in annual terms is still decelerating. For the year through last month, ADP’s estimate of private-sector employment rose 2.2%, fractionally below July’s pace and the slowest year-over-year advance since April 2014.

But let’s not overplay the deceleration card just yet. The current 2.2% annual increase is quite healthy and close to the best pace for the history of this series, which dates to 2001. The concern is that the slowdown in growth rolls on. Then again, maybe the annual rate will stabilize in the low-2% range.

All of which brings up an interesting if speculative possibility for the big-picture outlook: a relatively modest expansion that lays the groundwork for an unusually long phase of growth. One of the theories being kicked around these days is the notion that because the current growth phase for the US is modest, it will endure. Without the hazard of an overheating economy–far from it!–the Federal Reserve isn’t going to overplay its monetary hand any time soon and choke off growth, as it’s been known to do over the decades. Granted, the potential for a rate hike in the near-term future may suggest otherwise. But even if the rate hike starts this month (a debatable proposition at best), the Fed has made it clear that policy tightening will be slow and gradual.

In any case, as of last month, the US expansion is 74 months old, according to NBER.org data. That’s substantially longer than the post-war average of 58 months.

Some analysts reason that in the absence of stronger growth, the economy can continue to muddle forward for a relatively long period before suffering a new recession. To the extent that this theory is valid—a controversial idea at this stage—the price tag is a comparatively tepid expansion.

Given the recent market turbulence, such ideas have fallen on hard times. But the slow decline in the rate of employment growth still suggests that serious trouble isn’t on the immediate horizon.

Indeed, today’s ADP data implies that Friday’s official jobs report for August from the Labor Department will deliver mildly encouraging news. Econoday.com’s consensus forecast for the government’s estimate of nonfarm payrolls in August calls for a rise of 211,000—a touch above July’s 210,000 advance.

The bottom line: the case for seeing an imminent US recession remains a speculative proposition until (or if) the incoming figures tell us otherwise.