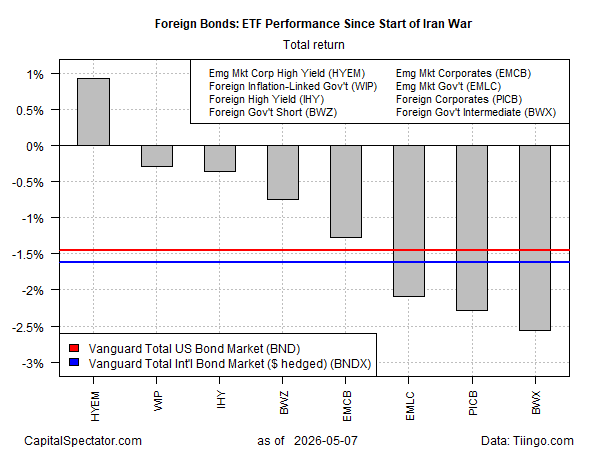

Diversifying into foreign bonds hasn’t provided much benefit to U.S. investors since the Middle East conflict began, with one exception: high‑yield corporate bonds issued by firms in emerging markets.

Bucking the trend since the conflict started on Feb. 28, the VanEck Emerging Markets High Yield Bond ETF (HYEM) is a rare bright spot in international fixed income from a US-dollar-based investment perspective. The fund is up 0.9% over this period, making it an outlier in a market otherwise marked by red ink.

HYEM’s performance stands out, though it generally mirrors the gains in U.S. junk bonds (JNK). By comparison, investment‑grade bonds—both corporate and government, in the US and abroad—are underwater since Feb. 28.

Why the disconnect? High‑yield bonds carry more risk than investment‑grade debt. One might have expected investors to flock to higher‑quality bonds as a safe haven and avoid junk bonds. Instead, the opposite has occurred.

One explanation: junk bonds have rallied as investors chase higher yields while war‑driven uncertainty eases, whereas investment‑grade bonds have lost ground amid rising interest‑rate expectations and inflation concerns.

Markets broadly began to rebound in late March. Initially, most bond sectors participated, but by mid‑April high‑yield and investment‑grade debt diverged sharply.

For example, HYEM has recovered all of its war‑related losses and even reached a new high earlier this week. A broad measure of U.S. investment‑grade bonds (BND)—including Treasuries and corporates—stalled in mid‑April and remains below its pre‑war close.

Analysts say high‑yield bonds have regained appeal thanks to their sizable coupons, which provide a meaningful yield cushion against market volatility. With fears of a worst‑case geopolitical escalation easing, investors have shown a renewed appetite for risk and rotated back into these higher‑return assets.

The divergence shows how quickly fixed‑income dynamics can shift when geopolitics and inflation collide. It also underscores why diversification across bond sectors matters—because in uncertain times, markets have a way of defying even the most confident forecasts.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno