Judging by the analysis in some circles, a recession is a forgone conclusion. More cautious types argue that the expansion continues, but just barely, and that a formal recession will likely start at some point in the next several months. As usual, it’s impossible to fully discount any given forecast. But a review of a broad range of economic and financial data still leaves room for debate. Yes, macro risk is rising for the US, but the economy has not yet reached the tipping point.

Let’s start with an indicator that’s animated recession chatter in recent days: the so-called Sahm rule. Named for economist Claudia Sahm, who developed the concept, the tipping point for recession is when the indicator rises 0.50 percentage points or more, based on a three-month average relative to the minimum of the three-month averages over the trailing 12 months. The current reading is 0.43 for June, which suggests that a formal recession warning could start as early as the next update for July.

The Sahm indicator has a strong track record and so its warning shouldn’t be dismissed. Nonetheless, relying on one indicator (informed solely by unemployment data in this case) is itself risky for the simple reason that no metric or model is flawless in business-cycle analysis. Indeed, it wasn’t that long ago that analysts praised the near-flawless track record of the Treasury yield curve as a reliable recession indicator. But more than a year-and-half after the curve inverted, the US economy has continued to expand.

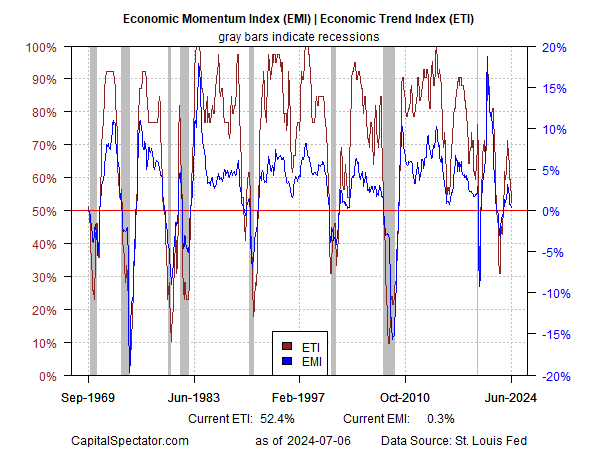

As always in calling recessions, the basic tradeoff is one of timeliness vs. reliability. Emphasizing one almost always requires degrading the other. The challenge is deciding how to balance the two. Focusing on that balancing act, and looking for the sweet spot in real time, is the goal of the The US Business Cycle Risk Report, a sister publication to CapitalSpectator.com. On that point, the newsletter’s modeling continues to highlight rising recession risk. As discussed in the current issue, a pair of proprietary, multi-factor business-cycle indicators have been signaling softer growth that’s moving closer to tipping points that signal an NBER-defined recession.

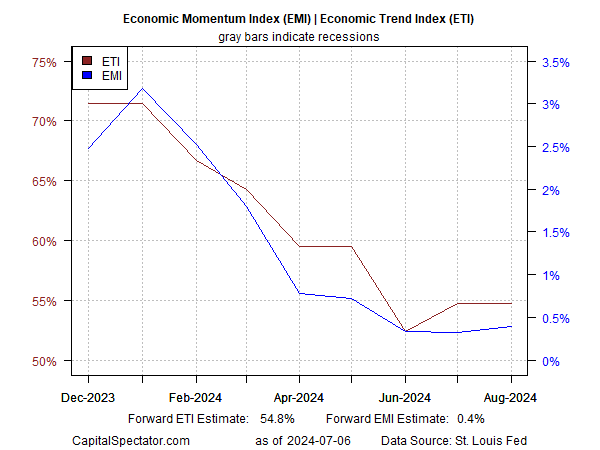

Nonetheless, near-term forward estimates of the two indicators shown above suggest that US economic activity is stabilizing, albeit at a slow/sluggish pace through August. The calculus could change, depending on incoming data, but for now the odds looks modestly favorable to slow/sluggish growth persisting for the immediate future.

Meanwhile, a review of other business cycle indicators points to relative strength in output. The Philly Fed’s ADS Index and the Dallas Fed’s Weekly Economic Index, for instance, are both reflecting a clear growth bias through the end of June.

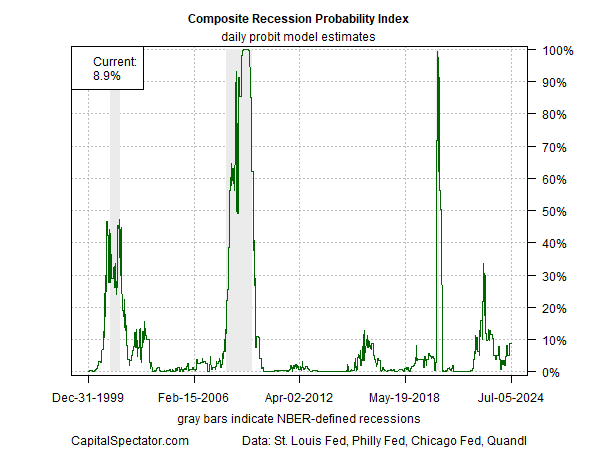

Aggregating several business-cycle benchmarks and estimating the implied recession-risk probability also reflects a modestly higher but still-low likelihood that an economic contraction has started or is imminent. The Composite Probability Recession Indicator – the primary benchmark for The US Business Cycle Risk Report – currently estimates a roughly 9% probability that the US economy is contracting or will contract in the very near future.

The bottom line: recession risk has risen, but it’s still premature to confidently declare that a downturn has started. Conditions could deteriorate in the weeks ahead, but for the moment slow/sluggish growth appears to be the odds-on favorite for the near-term outlook.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report