Trump announced new tariffs set to begin on Aug. 1. Imports from some of America’s biggest trade partners are targeted, including Japan and South Korea, which are set to face 25% tariffs, according to the President’s social media posts on Monday.

Trump announced new tariffs set to begin on Aug. 1. Imports from some of America’s biggest trade partners are targeted, including Japan and South Korea, which are set to face 25% tariffs, according to the President’s social media posts on Monday.

The week ahead will provide early clues for two very different risk factors looming for the bond market.

On the one hand, the on-again/off-again risk of tariffs is lurking – a development that could create new economic headwinds that soften growth and, in theory, lower interest rates as investors seek safe havens and the Federal Reserve eases its policy stance to provide stimulus. But tariffs could also lift inflation, perhaps persuading the Fed to keep rates higher for longer if not raise rates. Deciding which aspect of the tariff effect will dominate is tricky for several reasons, including ongoing ambiguity about when or if tariffs will change and uncertainty about the macro price tag associated wiht raising import costs.

US payrolls rose more than forecast in June, increasing 147,000 for the month. “The solid June jobs report confirms that the labor market remains resolute and slams the door shut on a July rate cut,” said Jeff Schulze, head of economic and market strategy at ClearBridge Investments. For the 1-year trend, payrolls effectively held steady at a 1.15% pace of growth, in line with gains in recent months.

When in the course of human events this week, it becomes necessary for yours truly to dissolve the usual routine and declare a particular truth to be self-evident: A long July 4 holiday weekend is an unalienable right, and so the Capital Spectator finds it necessary to declare independence from the office until the standard fare resumes on Monday, July 7. Happy Independence Day!

When in the course of human events this week, it becomes necessary for yours truly to dissolve the usual routine and declare a particular truth to be self-evident: A long July 4 holiday weekend is an unalienable right, and so the Capital Spectator finds it necessary to declare independence from the office until the standard fare resumes on Monday, July 7. Happy Independence Day!

The long-run expected total return for the Global Market Index (GMI) ticked higher for a third straight month in June, rising to an annualized 7.3% from the 7.2% estimate in the previous month. Today’s estimate is moderately below GMI’s realized 10-year performance. The forecast is calculated as the average of three models (defined below) for GMI, an unmanaged global benchmark that’s based on a market-value weighted mix of the major asset classes (excluding cash).

US job openings rose in May, reaching the highest level since November 2024. The increase surprised economists, who expected openings to decline. Despite the latest upturn, “We suspect underlying demand for new workers continues to recede amid growing signs of consumer spending fatigue,” said Sarah House, a senior economist at Wells Fargo.

Stocks in emerging markets extended their rally in June, posting the strongest gain for the major asset classes last month, based on a set of ETFs. A broad measure of US equities delivered a robust second-place performance amid rallies for all the main categories of global markets for the month.

The US dollar has fallen more than 10% year to date, the weakest start for a calendar year since 1973. The combination tariffs, inflation concerns and rising government debt are weighing on the greenback. The dollar’s slide is making investments in the US by foreigners more expensive. “A weaker dollar has become a crowded trade and I suspect the pace of decline will slow,” said Guy Miller, chief market strategist at insurance group Zurich.

For a brief few weeks it looked like the jig was up. But the selling wave has all but faded as sentiment has recovered and markets have rebounded from the perspective of a high-level global asset allocation perspective. Reviewing a select set of proxy ETFs suggests that risk-on sentiment has returned for the strategic outlook, based on prices through Friday’s close (June 27).

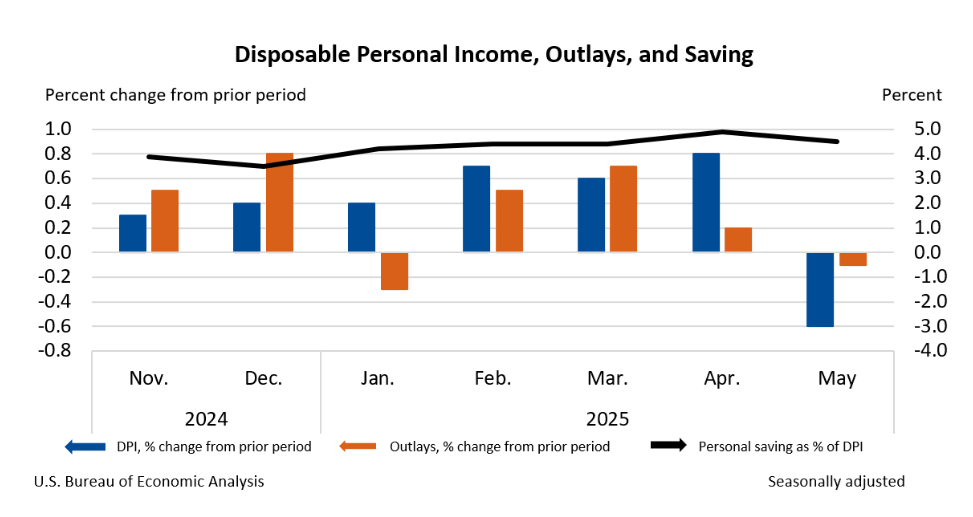

US consumer spending and income fell in May, the Bureau of Economic Analysis reported on Friday. Inflation also ticked up, based on core PCE. This measure of inflation, which is the Fed’s preferred benchmark for monitoring prices, edged up to a 2.7% year-over-year rate. “The report is a wash for the Fed and won’t alter its wait-and-see stance,” said Sal Guatieri, a senior economist at BMO Capital Markets. “The pullback in spending in May partly reflects payback from earlier tariff front-running, while the slightly warmer core price increase doesn’t settle the debate about how much tariffs will impact inflation.”