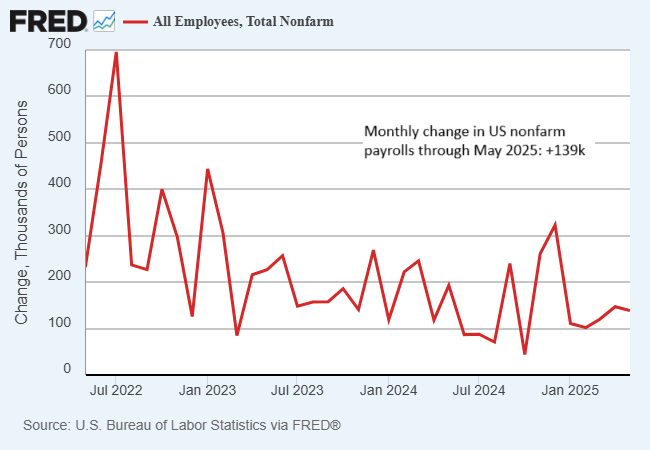

US payrolls rose more than expected in May. The economy added 139,000 jobs last month, the Labor Department reported. “Stronger than expected jobs growth and stable unemployment underlines the resilience of the US labor market in the face of recent shocks,” said Lindsay Rosner, head of multi-sector fixed income investing at Goldman Sachs Asset Management.