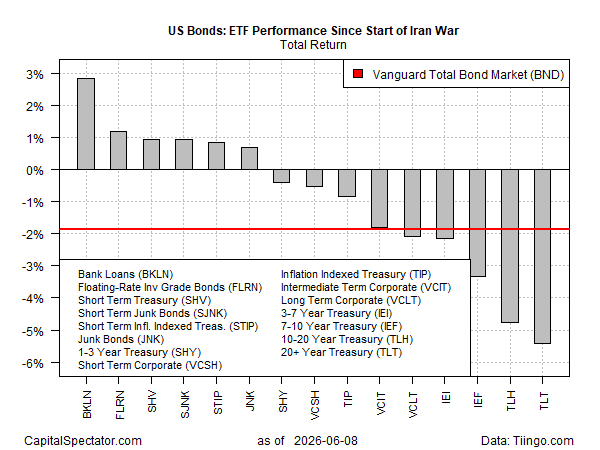

The search for higher yields continues to elevate the riskier facets of the bond market since the Iran conflict started. By contrast, most slices of the Treasury market remain underwater, based on a set of ETFs.

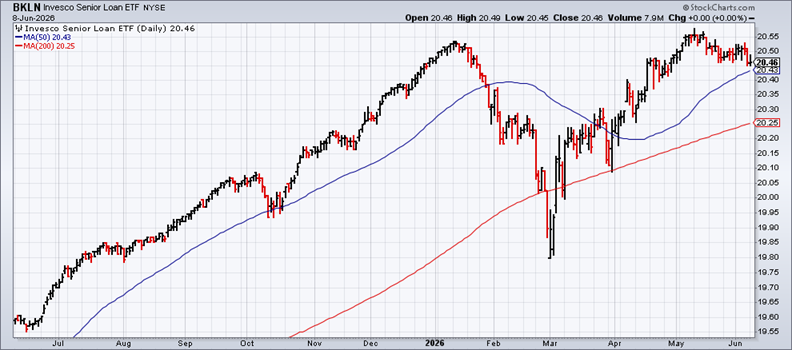

The leading performer by far since the crisis started on Feb. 28 is bank loans. The Invesco Senior Loan ETF (BKLN) is up 2.8% during this period, well ahead of the rest of the field.

The rest of the winners since Feb. 28: floating-rate securities (FLRN), a cash proxy (SHV), standard “junk” bonds (SJNK and JNK), and short-term inflation-indexed Treasuries (STIP). The remainder of the market is nursing losses, led by long Treasuries (TLT), which are currently posting a loss in excess of 5%.

What explains the performance divide? Treasuries are under pressure as inflation concerns lurk due to the run-up in the cost of energy. This spike has raised headline measures of prices and prompted forecasts that the Federal Reserve will be forced to raise interest rates later this year.

That’s hardly a bullish backdrop for fixed-income securities, yet bank loans and junk bonds have managed to post gains. One reason: private credit fundamentals remain strong despite recent market stress, according to Goldman Sachs. Defaults have been low and borrower performance solid. “The fundamentals of private credit still appear strong,” says Vivek Bantwal, global co-head of private credit at Goldman Sachs Asset Management.

Add in the higher yields and the package has been too good to ignore for investors. BKLN’s distribution yield is 6.61% (as of June 9), or nearly two percentage points above the long-bond’s current yield.

But the easy gains may be in the rearview mirror as the lingering inflationary effects of the Iran conflict continue to resonate. With no easy solutions on the horizon for a crisis that continues to keep Gulf energy exports low, the odds still look slim for a return to pre-war pricing pressure in the near term.

BKLN appears to be pricing in the shifting sentiment, driven by fading optimism for a quick end to the conflict and the macro blowback. The ETF is still comfortably ahead of the field since Feb. 28, but the recent peak looks like a ceiling for the foreseeable future without a material change in the outlook for a resumption in shipping through the Strait of Hormuz.

While markets are currently betting against a prolonged conflict, the latest news flow continues to challenge this forecast for the near term. Despite former President Trump’s calls for restraint, Israel and Iran’s recent strikes suggest that a resolution is still nowhere on the horizon.