The Middle East crisis appears no closer to resolution, underscored by Tuesday’s US military strikes on Iran. If recent history is a guide, the effects on the U.S. economy will be minimal, as today’s update on nowcasts for second‑quarter GDP suggests.

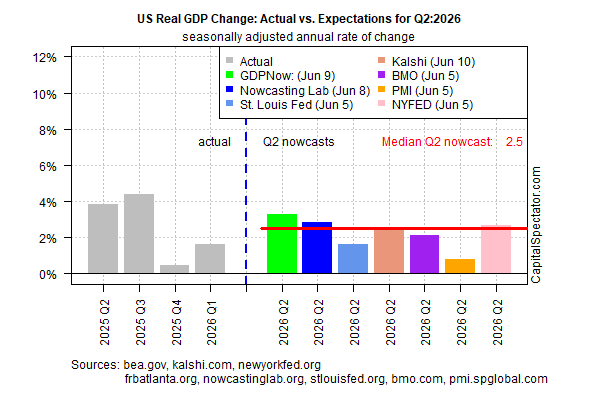

Growth for the April‑through‑June period continues to track at a 2.5% annualized rate, based on the median nowcast from several sources compiled by CapitalSpectator.com. The estimate points to a pickup in output over Q1’s modest 1.6% increase.

Today’s update is unchanged from last week’s estimate and suggests that the economy continues to accelerate following stall‑speed conditions in Q4, when GDP rose just 0.5%.

The history of the US economy since the war started on Feb. 28 has been a study in resilience. Over the past three months, economic activity has been largely unaffected by the Middle East conflict, with one glaring exception: inflation. It’s unclear whether rising pricing pressure will begin to unleash a deeper round of demand destruction, particularly in the consumer sector, but the effects so far have been modest.

One of the clearest signs of the economy’s strength: US payrolls rose at a robust pace for a third straight month in May.

“I think the job market, for the first time in a while, is moving in the right direction,” says Guy Berger, chief economist at small‑business payroll firm Homebase. “I wouldn’t call this a job market that’s quite ‘booming’—it’s certainly not as hot as the job market in ’21 and ’22—but it’s warming.”

The question is whether inflation will spoil the party in the second half of the year, forcing the Federal Reserve to raise interest rates and take initial steps toward removing the proverbial punch bowl, per the famous analogy by former Federal Reserve Chair William McChesney Martin to describe the central bank’s role in the economy.

Goldman Sachs reports: this week: “Our economists have not yet seen signs that the inflation shock from the war is broadening out — their composite indicator of the risk of more persistent inflation is still at a low level, although a jump in University of Michigan long‑term inflation expectations has pushed it slightly higher.”

The Fed is expected to leave its target rate unchanged at the upcoming meeting later this month, and again in July, based on Fed funds futures. Looking further out is as cloudy as ever and will remain so until something approximating a resolution to the Middle East crisis emerges.

For now, the numbers tell a story of an economy that refuses to flinch. The Q2 nowcast holds firm, signaling renewed momentum even as geopolitical risks swirl. Whether that strength endures into the second half will hinge on inflation’s next move — and on how long global tensions keep the outlook shrouded in fog.