A newly extended U.S.–Iran ceasefire and the reopening of the Strait of Hormuz are fueling cautious speculation that the conflict may be entering its final phase. The news will likely give financial markets a boost in the near term, assuming the agreement that the U.S. and Iran announced on Sunday holds.

Oil prices are already reflecting optimism. The U.S. benchmark is trading under $80 a barrel today for the first time in three months after President Trump and Iran’s Supreme National Security Council said a deal was reached to end the fighting and lift the blockades of the Strait of Hormuz that have prevented energy exports from the Gulf.

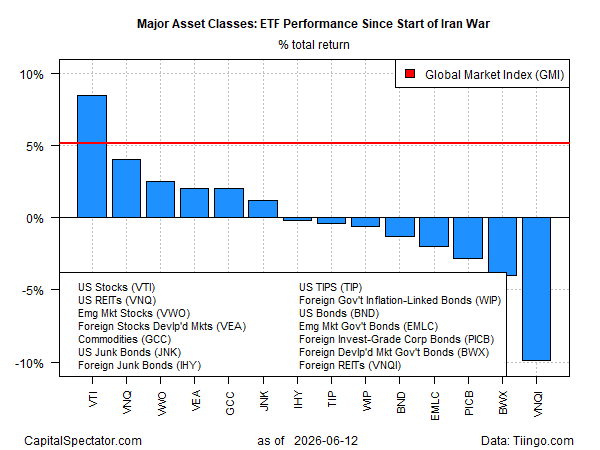

The major asset classes begin trading today with a wide range of performance results since the war started on Feb. 28. Using a set of ETFs highlights that U.S. equities (VTI) have been the performance leader, jumping nearly 8% since the conflict began. Global property shares ex‑U.S. (VNQI) have suffered the most among the major asset classes, slumping 10%.

The Capital Spectator’s Global Market Index (GMI) took a hit early in the war but began recovering in early April and has extended the rally to post a 5.2% gain over the course of the conflict. GMI is an unmanaged, market‑value‑weighted mix of the major asset classes (excluding cash) via ETF proxies and represents a competitive benchmark for globally diversified, multi‑asset‑class portfolio strategies.

A potential end to the U.S.–Iran conflict offers opportunity wrapped in uncertainty. If the war is over, the arrival of peace could unlock meaningful economic tailwinds. A durable ceasefire and a reopened Strait of Hormuz would reduce geopolitical risk in one of the world’s most critical energy corridors, easing pressure on oil prices, stabilizing shipping routes, and lowering volatility premiums across global markets. At the same time, the situation remains fragile: past de‑escalations between Washington and Tehran have unraveled quickly, and markets know that a single misstep can reverse gains overnight. It only takes one missile launch or drone attack to shatter expectations.

That combination of possible scenarios — real upside if calm holds, real downside if it doesn’t — is exactly why this moment feels like a rare but risky inflection point. One reason for caution is that the details of the peace deal have not yet been published. “Pre‑implementation discussions” are set for this week, followed by 60 days of technical talks on the thorny issue of Iran’s nuclear program.

Markets will be watching President Trump’s comments — and the reactions — at the G7 summit that starts today in France. For the moment, a new round of cautious optimism gives fresh hope that the biggest energy crisis in decades is now on track to wind down. But the multiple false dawns over the past several months suggest that time will be the ultimate arbiter of whether today’s headlines represent real progress or another display of fool’s gold.

“The global economy has experienced too much whipsawing in the past 100+ days of war to breathe easy based on a deal with no details,” advises Josh Lipsky, vice president and chair of international economics at the Atlantic Council and the senior director of the GeoEconomics Center. “The first test of those details will come as Trump is pressed by French President Emmanuel Macron and others gathered for the [G7] summit. Trump likely wanted to come to the meeting with a deal in place. Now he has set the terms for the leaders meeting — and they will be reacting to him.”

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report