The newly minted US–Iran ceasefire is only a day old, but markets reacted positively. Oil prices and Treasury yields fell, and stock prices surged in Monday’s trading. It’s encouraging early vote of confidence, although the economic effects of the war will linger and any rebound in energy exports from the Middle East will be gradual. That’s the best‑case scenario, which assumes that the US–Iran deal holds and inflation starts to ease.

The macro outlook may still be precarious, but the Federal Reserve is expected to leave its target rate unchanged at tomorrow’s policy announcement. The new Fed Chair, Kevin Warsh, will preside over his first FOMC meeting and press conference, where he’ll have a chance to reset the tone for expectations—for good or ill.

“Just given the novelty of the moment, because it’s Warsh’s first press conference, there’s really a lot of scope for what you might call a ‘market misinterpretation’ of his message,” says Kris Dawsey, head of economic research at the D.E. Shaw Group, a hedge fund. “It’s going to take some time for the market to really get calibrated on his communications.”

The Warsh era begins during an unsettled period for central banks. Several of the Fed’s counterparts have started raising interest rates, citing inflation as the catalyst.

The Bank of Japan today lifted its main interest rate to a 31‑year high. “After twenty years of deflation, Japan is now in an inflationary upcycle,” says Japan economist Jesper Koll. The European Central Bank raised interest rates last week for the first time since 2023. “We are beginning to see a broadening of inflation throughout the economy,” ECB President Christine Lagarde said, explaining that a “major energy shock” forced its hand.

The Fed, by contrast, is expected to maintain its wait‑and‑see strategy, effectively betting that the recent run‑up in US inflation will be temporary and begin to recede. Fed funds futures are pricing in near‑certainty that the bank will leave its target rate unchanged tomorrow at a 3.50%–3.75% range. Standing pat is also expected to prevail for the next several FOMC meetings.

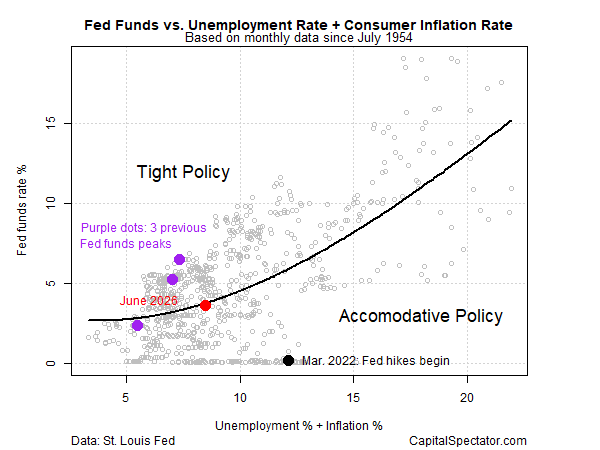

The Fed’s current policy stance is neutral, based on a simple model using inflation and unemployment. That’s a reasonable posture if inflation has peaked and will start to ease in the months ahead. The risk is that the Fed repeats the mistake of 2021–2022, when inflation surged and the central bank was slow to react.

The doves argue that core inflation remains relatively tame and well below the worrisome jump in headline measures, which reflect the sharp increase in energy prices.

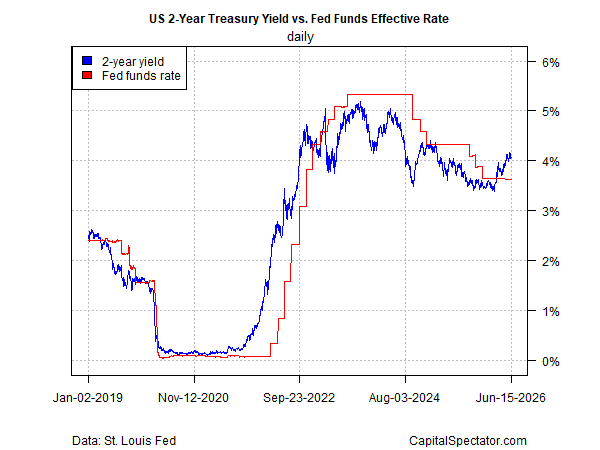

The Treasury market is effectively signaling that the Fed’s cautious approach to rate hikes is wrong. The policy‑sensitive 2‑year yield has climbed far above the median Fed funds rate, which implies expectations for near‑term rate hikes.

Chair Warsh will need to persuade markets that leaving policy steady is still a reasonable course. By contrast, the case for cutting rates—which President Trump has demanded—is far less defensible, if not reckless, at the moment.

The main challenge is that the macro dynamics likely to drive the direction of inflation in the months ahead are beyond the Fed’s power to influence through policy decisions. The key variable is the US–Iran peace deal, which will determine the pace of energy exports through the Strait of Hormuz.

The head of the world’s biggest tanker company says a rebound in shipping through the strait will take weeks at the earliest, as firms decide whether the US–Iran deal is “material,” says Jotaro Tamura, chief executive of Mitsui OSK Lines. Speaking with the FT, he advises:

“What will have to come in place is not just a simple agreement between the relevant countries, but it has to be material and translated into the real situations in the Strait of Hormuz, so that shipping lines can make themselves comfortable to go through.”

By leaving interest rates unchanged at tomorrow’s policy meeting, the Fed is essentially signaling that the Iran conflict is over, energy prices will continue to ease, and the inflationary threat has ended.

Tomorrow’s decision won’t settle the inflation debate, but it will set the tone. The Fed is betting on stability—now the world has to deliver it.