One of the biggest challenges for successfully managing asset allocation comes from a familiar source: you. There are many resources to tap for excelling on the technical side of portfolio management. From researching fund products to sorting market valuations to dissecting risk and return, there are countless analytical tools at your disposal in the information age. But no matter how many web sites you visit, no matter how many data points you crunch, managing your behavioral biases isn’t getting any easier.

That includes the tendency to see asset allocation as a collection of individual investments as opposed to one portfolio. This may not sound like a huge problem, but it is—if it keeps you from thinking strategically. The problem often starts if we’re emotionally tied to our investments. This is more likely with individual securities, but mutual funds and ETF purchases aren’t immune.

One of the more common hurdles is a form of mental accounting. For example, you’re inclined to think that because you bought a mutual fund at $20, you can never sell it—in whole or in part—at any price below that level.

We all fall into behavioral traps of one type or another, sometimes without realizing it. These traps aren’t always financially fatal, but biases of this kind almost always come with a cost: lower returns, higher risk, or both.

How can we defend ourselves? A good start is to routinely analyze your portfolio in holistic terms. This is critical because this information is extremely valuable and it’s not easy to see unless you’re looking for it. Let’s assume that you’ve carefully selected 10 ETFs for your asset allocation. No doubt you’re watching each one individually, as you should. But are you also monitoring how they behave collectively? In other words, are you routinely calculating the net asset value of your portfolio and running risk analysis on the overall portfolio? Are you comparing it with an appropriate benchmark, and periodically evaluating how your collective decisions have fared through time? Has your portfolio matched your expectations? Yes? Okay, why? Luck? Skill? A combination of both? If the results are disappointing, you should also look for satisfying answers in a bid to correct what’s been wrong.

Many investors aren’t focusing on these issues, in part because they’re too often focused on the pieces at the expense of the whole. But it’s the overall portfolio that defines success or failure, and so to minimize the holistic review is akin to driving with one eye closed. You may be ok, but you’re still courting disaster, and needlessly so.

As a visual example of what we’re facing when it comes to how we’re inclined to see investments, let’s imagine that we built an equally weighted portfolio of the major asset classes with representative ETFs. Here’s how the performances of the individual funds compare over the past year through yesterday, May 6:

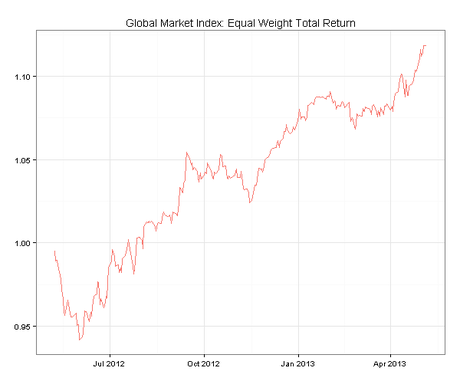

Our brains are inclined to see our investments as the chart above. But we also need to train ourselves to think like this:

The second chart is the equal-weighted portfolio performance of the 14 ETFs in the first chart. If we actually held this 14-fund portfolio, we would need to spend a fair amount of time with the underlying data in the second chart to answer critical questions about how our overall investment strategy stacks up.

The problem is that we’re predisposed to think and act as if the only perspective that matters is the first chart. The trees are important, but it’s essential that we don’t lose sight of the forest.

The solution, of course, begins by routinely calculating how your portfolio is performing and monitoring the results as if you held a single multi-asset-class investment product. This type of focus doesn’t come naturally to our brains, but with practice we can rewire our asset allocation thinking. In time, you’ll notice some productive changes, such as looking at individual funds and securities in terms of how they’ll impact the portfolio rather than focusing on the fund in isolation.

For some investors it’s easier to buy a multi-asset class fund, in which case the strategic focus is prepackaged as one ticker. Why go through the trouble of managing asset allocation directly and dealing with the messy parts? The rewards are potentially greater. From tax harvesting to exploiting volatility, taking direct control of your asset allocation provides a powerful foundation for enhancing results in risk-adjusted terms and perhaps on an absolute basis too. But first you’ll need an attitude adjustment.