US macro risk has eased in recent days, thanks to a mix of upbeat economic reports and a rebound in financial markets. The potential for trouble is still elevated relative to the outlook during last year’s fourth quarter. But for the moment, the numbers generally look a bit less threatening compared with the steady drumbeat of warnings in previous weeks.

It’s unclear if this week’s step back from the brink marks a genuine turning point that leads to stronger growth–or is it a temporary reprieve that will soon give way to even darker results? No one really knows, of course, although the numbers published through yesterday (Feb. 17) certainly paint a modestly brighter profile compared with recent history.

One thing that’s remained constant is the lack of a clear-cut recession warning in The Capital Spectator’s proprietary business-cycle benchmarks. A markets-based view of the macro trend has assumed the worst, but so far there’s still no confirmation in a broad reading of the economic data. Yesterday’s update of the Philly Fed’s ADS Index, another measure of the macro trend, aligns with the view that the near-term outlook still looks positive. That’s also the message in yesterday’s revised nowcast for first-quarter GDP growth via the Atlanta Fed’s GDPNow model. The bank’s Feb. 17 data projects that the US economy will expand by 2.6% (seasonally adjusted annual rate) in the first three months of this year. If accurate, the economy is on track to accelerate after posting a tepid 0.7% GDP increase in last year’s Q4.

There’s still plenty to worry about, of course, including sluggish growth for the global economy. The US is relatively insulated from offshore blowback, but the weakness in foreign economies–China and emerging markets in particular–is certainly a risk factor, and perhaps one that will bring stronger headwinds in the months ahead. On that note, consider that the OECD today reduced its outlook for economic activity this year. Global GDP is now on track to rise by 3.0% in 2016–0.3 percentage points lower than the group’s November forecast. “Global growth prospects have practically flat-lined, recent data have disappointed and indicators point to slower growth in major economies, despite the boost from low oil prices and low interest rates,” OECD Chief Economist Catherine Mann advised.

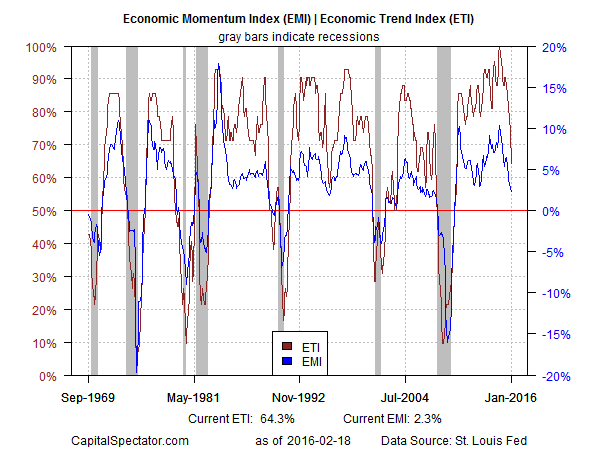

The good news is that a broad reading of the numbers published to date still imply that the US will skirt a new recession, based on a methodology outlined in Nowcasting The Business Cycle: A Practical Guide For Spotting Business Cycle Peaks. The Economic Trend and Momentum indices (ETI and EMI, respectively) have fallen in recent months but remain at levels that equate with expansion. Here’s a summary of recent activity for the components in ETI and EMI:

Aggregating the current data in the table above into business cycle indexes reflects weaker but still positive trends overall. The latest numbers for ETI and EMI indicate that both benchmarks are above their respective danger zones: 50% for ETI and 0% for EMI. Yet it’s also clear that both indexes have tumbled sharply in recent months. When/if the indexes fall below the tipping points, we’ll have clear warning signs that recession risk is at a critical level. Meantime, the latest updates for January show that ETI is 64% and EMI is 2% — i.e., there’s still a margin of safety, albeit a relatively narrow one between current values and the danger zones, as shown in the chart below. (See note at the end of this post for ETI/EMI design rules.)

Translating ETI’s historical values into recession-risk probabilities via a probit model also points to low business cycle risk for the US through last month. Analyzing the data with this methodology shows a slight uptick in risk lately, but the numbers still imply that the odds are virtually nil that the National Bureau of Economic Research (NBER) — the official arbiter of US business cycle dates— will declare January as the start of a new recession.

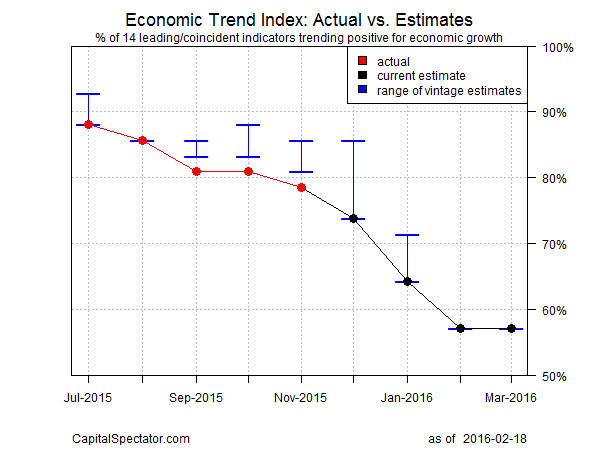

For another perspective, consider how ETI may evolve as new data is published. One way to project future values for this index is with an econometric technique known as an autoregressive integrated moving average (ARIMA) model, based on calculations via the “forecast” package for R, a statistical software environment. The ARIMA model calculates the missing data points for each indicator, for each month–in this case through Mar. 2016. (Note that Nov. 2015 is currently the latest month with a complete set of published data.) Based on today’s projections, ETI is expected to remain above its danger zone for the near term. Nonetheless, the near-term projections call for a decline that’s only modestly above the 50% mark, which suggests that business-cycle risk may soon approach the tipping point. (Keep in mind that frequent business cycle updates are available throughout each month in The US Business Cycle Risk Report.)

Forecasts are always suspect, of course, but recent projections of ETI for the near-term future have proven to be relatively reliable guesstimates vs. the full set of published numbers that followed. That’s not surprising, given the broadly diversified nature of ETI. Predicting individual components, by contrast, is prone to far more uncertainty in the short run. The current projections (the four black dots on the right in the chart above) suggest that the economy will continue to expand. The chart above also includes the range of vintage ETI projections published on these pages in previous months (blue bars), which you can compare with the actual data that followed, based on current numbers (red dots). The assumption here is that while any one forecast for a given indicator will likely miss the mark, the errors may cancel out to some degree by aggregating a broad set of predictions. That’s a reasonable assumption via the historical record for the ETI forecasts.

For additional perspective on judging the track record of the forecasts, here are the previous updates for the last three months:

21 Jan 2016

18 Dec 2015

19 Nov 2015

Note: ETI is a diffusion index (i.e., an index that tracks the proportion of components with positive values) for the 14 leading/coincident indicators listed in the table above. ETI values reflect the 3-month average of the transformation rules defined in the table. EMI measures the same set of indicators/transformation rules based on the 3-month average of the median monthly percentage change for the 14 indicators. For purposes of filling in the missing data points in recent history and projecting ETI and EMI values, the missing data points are estimated with an ARIMA model.