Economic growth is expected to accelerate in this week’s initial estimate of fourth-quarter gross domestic product (GDP). The Bureau of Economic Analysis appears set to report a strong rebound in output for Q4 in Thursday’s release (Jan. 27). But the recovery will be short-lived, based on recent downgrades for the US outlook in early 2022.

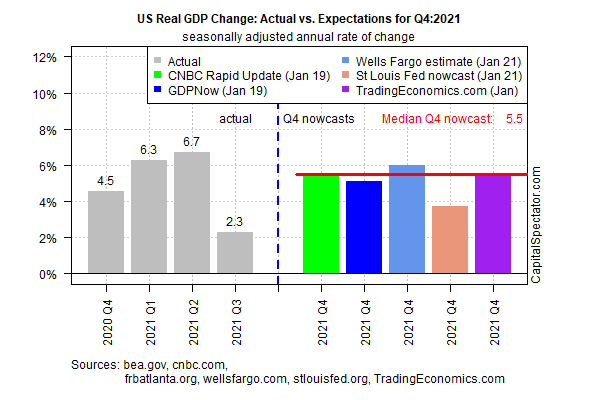

Let’s start with the good news. The preliminary estimate of GDP for Q4 is on track to post a strong 5.5% advance (seasonally adjusted annual rate), based on the median estimate for a set of nowcasts compiled by CapitalSpectator.com. The expected gain marks a sharp improvement over Q3’s 2.3% increase.

Today’s Q4 estimate has been revised down from the previous nowcast, but the upbeat outlook continues to reflect a robust improvement in economic activity compared with Q3’s modest increase.

The acceleration appears to be fading quickly in the new year, however, as headwinds strengthen. Several recent estimates for Q1 GDP point to a sharp slowdown. Now-casting.com, for example, has revised its Q1 nowcast down to a weak 1.7% rise for the January-through-March period. That compares with a 3.2% nowcast for Q1 at the start of the year.

Newly published sentiment data points to an even weaker reading. Yesterday’s release of the US Composite PMI Output Index (a GDP proxy) shows the economy slowing to a crawl in January.

“Soaring virus cases have brought the US economy to a near standstill at the start of the year, with businesses disrupted by worsening supply chain delays and staff shortages, with new restrictions to control the spread of Omicron adding to firms’ headwinds,” advises IHS Markit.

Weaker economic activity is also showing up in other business-cycle benchmarks. The Philly Fed’s ADS Index, a real-time measure of business conditions, eased in mid-January to its lowest reading since September. Although the ADS data still reflects expanding economic activity, the latest downturn is another reminder that a downside bias dominates the macro trend in early 2022.

The positive spin is that the sharp slowdown may soon reverse later in the year, perhaps as early as Q2. One clue for thinking so: “resilient” demand, IHS Markit reports. “New orders for goods and services continued to rise strongly, albeit registering the weakest rise since December 2020. The resulting gap between output and new orders was the second largest recorded by the survey to date, exceeded in the last 12 years only by the gap seen in October 2013, reflecting the near-unprecedented constraints on output recorded in January due to the flare up of COVID-19 cases and accompanying virus containment precautions.”

For the immediate future, however, economists are reducing growth estimates for early 2022. The main culprit: the resurgence of pandemic-related fallout.

“Omicron’s fingerprints” are found on the reduced expectations for this year’s start, says Constance Hunter, chief economist for the accounting firm KPMG. “It will slow growth in the beginning of the first quarter.”

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report