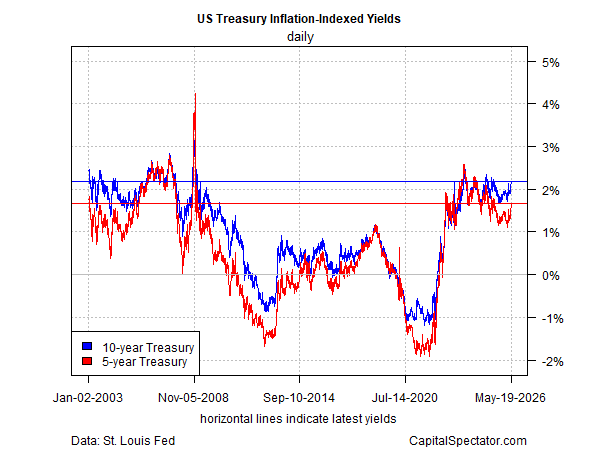

The 10‑year real US Treasury yield is hovering near a 20‑year high, with the 5‑year not far behind. Whether this is a good moment to lock in inflation‑indexed yields may hinge on how the Gulf crisis evolves in the months ahead.

The recent surge in Treasury yields has strengthened the case for holding bonds, and real yields are no exception. After years of volatility—including a plunge into negative territory during the pandemic followed by a sharp rebound driven by the Federal Reserve’s rate hikes—real yields are now back in ranges last seen two decades ago. The 10‑year TIPS yield stands at 2.18%, offering a guaranteed real return if held to maturity.

That’s an appealing level by historical standards. For comparison, the nominal 10‑year yield (without inflation protection) reached 4.67% on May 19, implying a market‑based inflation expectation of 2.49%—near a three‑year high, though below the brief 3.0% peak in 2022.

Whether it makes sense to lock in today’s real yields depends on where rates go next, and that path is unusually uncertain. The dominant near‑term driver remains the Middle East crisis.

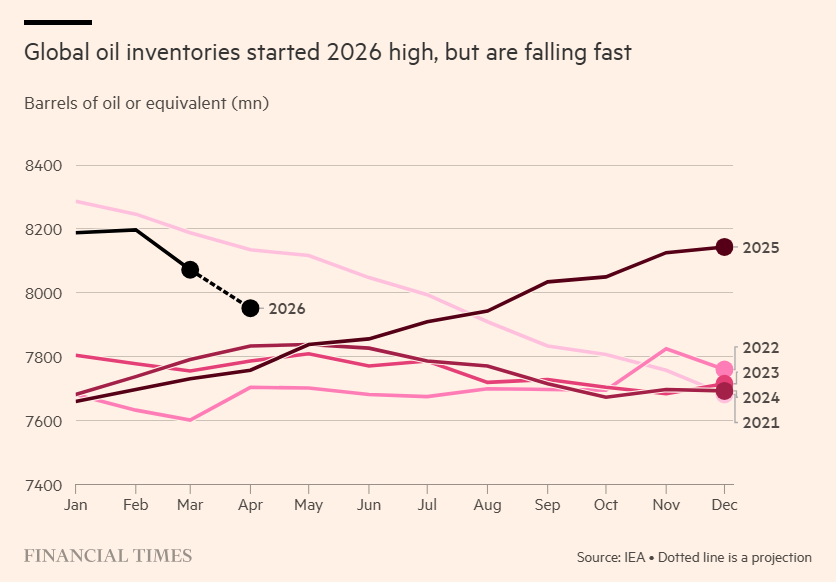

A rapid resolution that reopens the Strait of Hormuz and restores energy flows would likely ease inflation fears and push yields lower. But that outcome still appears unlikely. Fatih Birol, head of the International Energy Agency, warned Monday that commercial oil inventories are falling quickly, with only weeks of supply left as the Iran war and the Strait’s closure choke shipments. Strategic reserves have helped offset lost exports, but, as he noted, they “are not endless.”

Global inventory data suggests the supply‑demand squeeze will worsen if the stalemate persists, according to a chart from the Financial Times.

Meanwhile, geopolitical tensions remain high. President Trump said Monday he was “an hour away” from ordering new strikes on Iran before Gulf allies urged restraint. Iran’s Revolutionary Guard responded that any renewed attacks by the US or Israel would expand the conflict “beyond the region,” with retaliation in “places you cannot imagine,” according to Mehr News.

In a worst‑case scenario—renewed war, higher energy prices, and rising inflation—the bond market would likely demand an even higher risk premium, pushing yields up further. In a best‑case scenario—de‑escalation and resumed exports—yields could fall.

Given the uncertainty in the current climate, it’s difficult to predict the path ahead with confidence. That argues for a balanced approach: allocating part of a bond portfolio to TIPS to capture elevated real yields while keeping some cash available to respond to further market stress.

Unless one is unusually confident about both the outcome and timing of events in the Middle East, hedging across multiple scenarios has rarely looked more sensible.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report