In a mixed year for equity risk factors, several flavors of large-cap shares stand out as this year’s winners, based on a set of ETF proxies through Monday’s close (Dec. 4). Small-cap stocks are on track to trail by a wide margin in relative terms for the calendar year, but the recent rally in this corner is inspiring new forecasts that this slice of equity risk premium is poised to outperform in the new year.

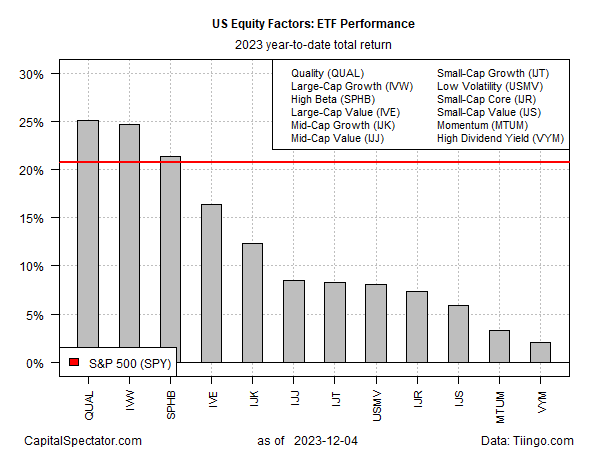

For 2023, however, the die looks cast for the theme that bigger is better from a performance perspective. Leading the equity factor field with roughly 25% year-to-date gains: iShares MSCI USA Quality Factor ETF (QUAL), a large-cap growth fund that targets so-called quality stocks, and iShares S&P 500 Growth ETF (IVW). On both fronts, these ETFs are well ahead of the gains for other equity factors and the standard US equity benchmark via SPDR S&P 500 ETF (SPY), which is large-cap biased as well.

The weakest equity factor this year: a strategy of targeting relatively high dividends via Vanguard High Dividend Yield Index Fund (VYM), which is posting a tepid 2% rise so far in 2023.

The recent rally in small cap shares is focusing minds anew on the possibility that this corner of the equities market may be primed to outperform in the new year. Although iShares Core S&P Small-Cap ETF (IJR) has been a laggard this year, the fund is up more than 9% in the past month, dramatically outperforming the broad market (SPY) a sizable margin. A lot of the outperformance has come in recent days via a surge in IJR.

It’s premature to read too much into the small-cap gains, but the basis for thinking positively for this slice of the market is linked with rising expectations for lower interest rates next year, an outcome that analysts say would be especially beneficial for smaller firms.

“For smaller stocks, which trade like call options to distant earnings, lower interest rates make these earnings more valuable when discounted to the present,” writes Panos Mourdoukoutas, a professor of economics at LIU Post in New York.

There’s also the valuation argument. A month ago Ed Clissold, chief U.S. strategist at Ned Davis Research, advised that “small caps are trading at near their steepest discount on record.”

Bill Brewster, a research analyst at Sullimar Capital Group, notes this week that “small caps have been decimated” across the board, which lays the groundwork for finding diamonds in the rough. “That’s got to be a good hunting ground in general right now, because they have not reflated all the way.”

Indeed, comparing small caps (IJR) to the broad market (SPY) paints a clear picture of the wide divergence in performance this year.

The question is whether the latest pop in small caps is noise? Indeed, there have been several false flags for IJR in recent history and so it’s not yet clear that the latest run is the genuine article. But using hedge funds as a guide suggests a turning point may be brewing.

Reuters reports: “Hedge funds cut their exposure in equities, mainly in healthcare, while adding a bit of small-cap stocks to their portfolios last week, according to a BofA Securities note about its clients flow trends.”

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno