● The Problem of Twelve: When a Few Financial Institutions Control Everything

John Coates

Summary via publisher (Columbia Global Reports)

A “problem of twelve” arises when a small number of institutions acquire the means to exert outsized influence over the politics and economy of a nation. The Big Four index funds of Vanguard, State Street, Fidelity, and BlackRock control more than twenty percent of the votes of S&P 500 companies—a concentration of power that’s unprecedented in America. Then there’s the rise of private equity funds, such as the Big Four of Apollo, Blackstone, Carlyle, and KKR, which have amassed $2.7 trillion of assets, and are eroding the legitimacy and accountability of American capitalism—not by controlling public companies, but by taking them over entirely, and removing them from public disclosure and scrutiny. This quiet accumulation in the last few decades represents a dramatic transformation in how the American economy operates—a sea change that few of us have noticed and all of us need to consider. Harvard law professor John Coates forcefully calls our attention to what is sure to be one of the major political and economic issues of our time.

Author Archives: James Picerno

Research Review | 18 August 2023 | Factor Risk Premia Analysis

Expanding the Fama-French Factor Model with the Industry Beta

Anatoly B. Schmidt (NYU Tandon School of Engineering)

August 2023

Recently it was shown that the news-based stock pricing model (NBSPM) outperforms the momentum-enhanced five-factor Fama-French model (FF5M) for a representative list of holdings of the major US equity sector ETFs both in-sample (Schmidt 2023) and out-of-sample (Schmidt 2022). The leading term in NBSPM besides the market (CAPM) beta is the industry beta estimated using returns of the relevant equity sector ETFs or industry ETFs. In this work, the industry beta is added to FF5M. It is found that the resulting model (FF5MI) is generally more accurate in-sample than NBSPM in terms of the mean squared error but not necessarily in terms of the mean absolute error. However, FF5MI is always inferior to NBSPM out-of-sample. This implies that the industry beta has the major impact on stock prices while the FF5M factors may yield an over-fitted model.

Macro Briefing: 18 August 2023

* Markets starting to realize that interest rates could stay higher for longer

* US Leading Economic Index for July continues to forecast elevated recession risk

* Philly Fed Mfg Index rebounds in August, hints at recovery for sector

* China property developer Evergrande files for bankruptcy in US

* US jobless claims edge down, continue to indicate labor market resiliency:

US Recession Risk For Q3 Continues To Fade

It’s been clear for some time that US recession risk has been sliding in recent months, but this week’s updates of a widely followed GDP nowcast published by the Atlanta Fed has been revised up – a lot – for the third quarter. According to this model, the US economy isn’t just rolling along at a moderate pace — it’s surging.

Macro Briefing: 17 August 2023

* Fed minutes minutes show officials see ‘upside risks’ to inflation

* More rate hikes possible, says former Fed Governor Randall Kroszner

* Atlanta Fed GDPNow model’s nowcast for US Q3 GDP surges to +5.8%

* Business inflation expectations fall “significantly” to 2.5% in Aug: Atlanta Fed

* China housing slump worse than official data show, according to property agents

* US industrial output rebounds sharply in July after two months of decline

* US housing construction recovers with strong gain in July

* 10-year US Treasury yield rises to 4.28%, highest in 15 years:

Has Treasury Market Misjudged Timing For Peak Rates… Again?

For much of the year the bond market has been embracing expectations that the Federal Reserve’s interest rates increases have peaked, or were about to peak. The underlying logic centered on the ongoing slide in inflation following 2022’s spike. Inflation has continued to ease, but the market has continually discovered that the future’s still uncertain as the Fed pushed ahead with more hikes.

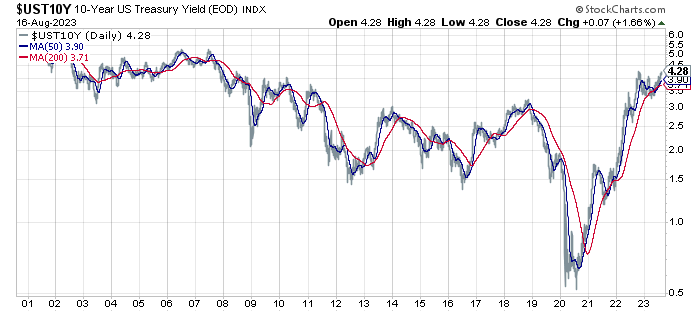

Macro Briefing: 16 August 2023

* Fed official says “I think we’re a long way away from cutting rates”

* US real Treasury yields approach 14-year high

* China home prices drop for second month in July as sector’s headwinds build

* US homebuilder sentiment eases in August–first setback in 10 months

* New York Fed manufacturing activity fell more than forecast in August

* US retail sales rise more than forecast in July, advancing for fourth month:

Early US Q3 GDP Nowcasts Point To Ongoing Economic Growth

Recession forecasts continue to swirl in some corners of the economics profession, but early econometric estimates for third-quarter GDP data suggest that the expansion will persist for now.

Macro Briefing: 15 August 2023

* Why did so many economists miss the “big disinflation”?

* Japan’s economic growth roars back in Q2 as exports surge

* China announces surprise interest rate cut amid struggling economy

* China halts publishing youth jobless rate data after it hits record high of 20%

* Wall Street sees low-priced commercial real estate as investment opportunity

* Fitch says it may downgrade dozens of banks, including JPMorgan Chase

* Russia’s central bank lifts interest rates sharply to combat sliding ruble

* 10-year US Treasury yield ticks up to 4.19%, highest since late-2022:

Global Rally Stalls, Pulling More Markets Into Red For 2023

Most of the world’s markets are still posting sizable gains year to date, but the recent selling has claimed another victim for the loss column. As of Friday’s close, three of the 14 slices of the major asset classes are now underwater this year, based on ETF proxies through through Friday, Aug. 11. Two weeks ago, all the major asset classes were enjoying gains in 2023.