Yesterday’s ADP estimate on US private payrolls in July was a bit of a disappointment. Companies added 185,000 workers last month—the smallest gain in three months. The news implies that tomorrow’s official jobs report from Washington for July will also reflect softer growth. Is the weaker-than-expected increase a sign that the labor market’s cooling? Maybe, although the latest ISM Non-Manufacturing survey numbers for July suggests that the services sector, the primary source of US employment, is still adding new jobs at a strong pace. In other words, last month’s softer payrolls report via ADP is mostly due to manufacturing—the energy sector in particular, which is reeling from sharply lower commodity prices. The broad trend for US employment, however, continues to look encouraging, courtesy of the upbeat numbers in services.

Continue reading

Initial Guidance | 6 August 2015

● ADP: US private-job growth slows in July

● ISM: US services-sector growth accelerates in July

● US Services PMI strengthened in July

● US trade gap rises 7% in June on stronger imports

● PMI: global economic growth ticked higher in July

● Eurozone retail PMI surges to 4-year high in July

● German factory orders surged in June

● UK industrial production is surprisingly weak in June

ADP: Softer-Than-Expected Rise For US Private Payrolls In July

Payrolls for US companies increased by a seasonally adjusted 185,000 in July, which is moderately below Econoday.com’s consensus estimate for a 210,000 advance. The gain marks the smallest rise in three months, according to this morning’s release of the ADP Employment Report. Meanwhile, the year-over-year pace continued to weaken, sliding to a 2.26% gain for the year through last month—the slowest annual growth rate in more than a year.

Continue reading

Health Care & Energy: US Sector Momentum At The Extremes

The US stock market has witnessed its share of turbulence in recent months, but the jump in price volatility hasn’t dented the leadership role of the health care sector. At the opposite extreme: energy companies continue to dominate the field in the category of downside momentum.

Continue reading

Initial Guidance | 5 August 2015

● US factory orders rise in June–first increase in 3 months

● US small-business borrowing rises to record in June

● Redbook: US retail sales advance in July

● CoreLogic’s US Home Price Index surges 6.5% for year through June

● Eurozone retail sales sharply lower in June

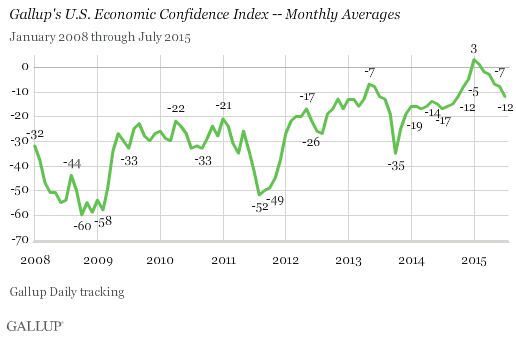

● Gallup’s US Economic Confidence Index falls to 9-month low in July

ADP Employment Report: July 2015 Preview

Private nonfarm payrolls in the US are projected to increase by 227,000 (seasonally adjusted) in tomorrow’s July update of the ADP Employment Report, based on The Capital Spectator’s average point forecast for several econometric estimates. The average projection is modestly below June’s increase.

Continue reading

Risk Premia Forecasts | 4 August 2015

The expected risk premium for the Global Market Index (GMI) ticked up in July, touching a two-month high. GMI — an unmanaged, market-value weighted mix of the major asset classes — is projected to earn an annualized 3.7% over the “risk-free” rate in the long term. (For details on the equilibrium-based methodology that’s used to generate the forecasts each month, see the summary below). Today’s updated estimate, which is based on data through the close of last month, increased 10 basis points from the previous projection.

Continue reading

Initial Guidance | 4 August 2015

● US personal spending +0.4% and income +0.2% in June

● US auto sales surge 5.3% in July

● ISM: US manufacturing growth ticks down in July

● US construction spending rises by a sluggish 0.1% in June

● Gallup: US consumer spending flat in July

Major Asset Classes | July 2015 | Performance Review

A partial rebound was in play in July after widespread losses dominated the global markets during the previous two months. Notably, last month witnessed a sharp increase in US real estate investment trusts (REITs)–the first increase after three monthly declines. Stock markets in the developed world were mostly higher in July as well. But July was no stranger to selling in some corners, including hefty declines in emerging-market stocks and bonds and a dramatic slide in commodities overall.

Continue reading

Initial Guidance | 3 August 2015

● US employment costs decelerated sharply in Q2

● US consumer sentiment softens more than expected in July

● Puerto Rico misses bond payments over the weekend

● PMI: Eurozone manufacturing output rises “solidly” in July

● PMI: manufacturing decline in China accelerates in July

● Greek stock market crashes on Monday after 5-week shutdown