American shares suffered their deepest weekly decline in more than a year last week, but the setback wasn’t enough to dethrone US stocks as the world’s top-performing asset class in 2024. Based on a set of ETFs tracks the major asset classes through Friday’s close (Sep. 6), US equities are still leading the field by a wide margin.

Macro Briefing: 9 September 2024

US payrolls rebounded in August, but the 142,000 increase in new jobs was less than forecast. “The labor market is cooling at a measured pace,” notes Jeffrey Roach, chief economist at LPL Financial. “Businesses are still adding to payrolls but not as indiscriminately. The Fed will likely cut by 25 basis points and reserve the right to be more aggressive in the last two meetings of the year.” The unemployment rate dipped to 4.2% from 4.3% previously. Although that’s modest relative to the history, the recent increase has triggered recession warnings, according to some analysts. “The increased unemployment rate is in a range where we have historically been in recessions,” says economist Claudia Sahm. “But that’s a history, that’s a past. We’re not in a recession right now, but we do have a weakening labor market.”

Book Bits: 7 September 2024

● The Greatest of All Plagues: How Economic Inequality Shaped Political Thought from Plato to Marx

● The Greatest of All Plagues: How Economic Inequality Shaped Political Thought from Plato to Marx

David Lay Williams

Summary via publisher (Princeton U. Press)

Economic inequality is one of the most daunting challenges of our time, with public debate often turning to questions of whether it is an inevitable outcome of economic systems and what, if anything, can be done about it. But why, exactly, should inequality worry us? The Greatest of All Plagues demonstrates that this underlying question has been a central preoccupation of some of the most eminent political thinkers of the Western intellectual tradition.

Research Review | 6 September 2024 | Portfolio Risk Management

Semivolatility-managed portfolios

Daniel Batista da Silva (U. of Geneva) and M. Fernandes (Getulio Vargas Fnd.)

July 2024

There is ample evidence that volatility management helps improve the risk-adjusted performance of momentum portfolios. However, it is less clear that it works for other factors and anomaly portfolios. We show that controlling by the upside and downside components of volatility yields more robust risk-adjusted performances across a broad set of factors and anomaly portfolios, as well as exchange-traded funds. In particular, we propose semivolatility-managed portfolios that, apart from deleveraging when downside volatility is high, also exploit the higher expected returns in times of good volatility. We find that our semivolatility-managed portfolios that control for both skewness and downside volatility perform better than the original portfolios and extant (semi)volatility management proposals.

Macro Briefing: 6 September 2024

US hiring at companies slowed again in August, dipping to a rise of 99,000 over the previous month, according to the ADP Employment Report. The downshift marks the softest pace since January 2021. “The job market’s downward drift brought us to slower-than-normal hiring after two years of outsized growth,” says Nela Richardson, chief economist, ADP. “The next indicator to watch is wage growth, which is stabilizing after a dramatic post-pandemic slowdown.”

Will Friday’s Jobs Report Alter The Upbeat Q3 GDP Nowcast?

The current lineup of US GDP nowcasts for the third quarter continue to indicate a softer but still solid growth rate. Wall Street is wondering if the upcoming payrolls report for August will change the calculus.

Macro Briefing: 5 September 2024

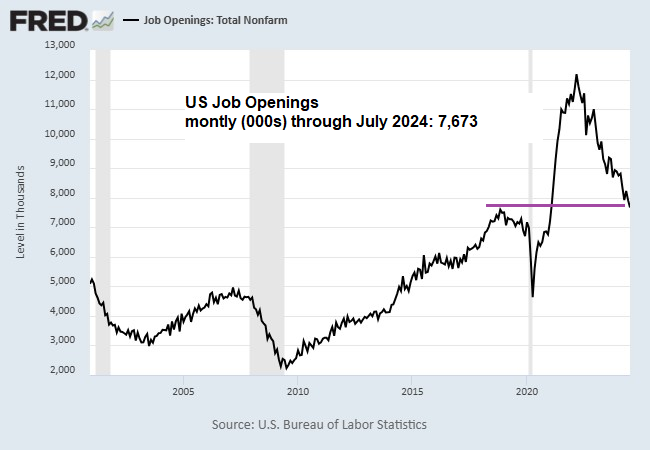

US job openings in July fell to the lowest level since January 2021, the Labor Department reports. The slide highlights concerns that the labor market’s recent slowdown will continue. The report also strengthens the view that the Federal Reserve will cut interest rates at next week’s policy meeting (Sep. 18). “The labor market is no longer cooling down to its pre-pandemic temperature, it’s dropped past it,” says Nick Bunker, head of economic research at the Indeed Hiring Lab. “Nobody, and certainly not policymakers at the Federal Reserve, should want the labor market to get any cooler at this point.”

Total Return Forecasts: Major Asset Classes | 04 September 2024

A revised long-term performance forecast for the Global Market Index (GMI) fell again in August. The downshift marks a second straight decline in expected return for GMI, an unmanaged benchmark that holds all the major asset classes (except cash) according to market weights via a set of ETF proxies.

Macro Briefing: 4 September 2024

US manufacturing activity continued to contract in August, according to survey data released for the ISM Manufacturing Index. The benchmark ticked higher last month but reflected contraction for the fifth straight month and for the 21st time in the last 22 months. The report also showed that manufacturers continue to pay higher prices for inputs. “Input price pressures moved up modestly to the highest in three months, but they are not so high in our judgment to threaten continued slow disinflation,” says Conrad DeQuadros, senior economic advisor at Brean Capital. “No bar to a September rate cut here but nothing to push the Fed to a half-point cut either.”

Major Asset Classes | August 2024 | Performance Review

US real estate investment trusts led global markets higher for a second straight month in August, based on set of ETFs representing the major asset classes. Another performance redux: commodities were the outlier, posting the only monthly loss, echoing the setback in July.